Advertisement

- New Zealand

- /

- Building

- /

- NZSE:FBU

We Think Some Shareholders May Hesitate To Increase Fletcher Building Limited's (NZSE:FBU) CEO Compensation

Performance at Fletcher Building Limited (NZSE:FBU) has been reasonably good and CEO Ross Taylor has done a decent job of steering the company in the right direction. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 25 October 2022. However, some shareholders will still be cautious of paying the CEO excessively.

Our analysis indicates that FBU is potentially undervalued!

How Does Total Compensation For Ross Taylor Compare With Other Companies In The Industry?

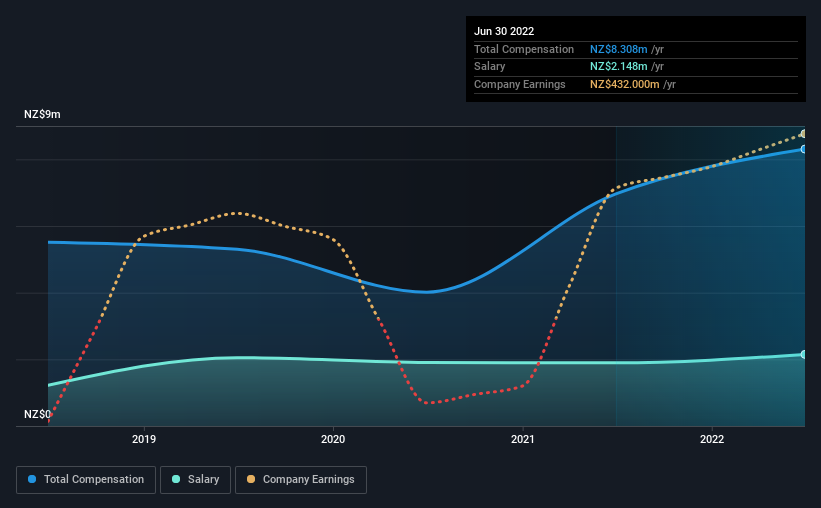

According to our data, Fletcher Building Limited has a market capitalization of NZ$4.0b, and paid its CEO total annual compensation worth NZ$8.3m over the year to June 2022. Notably, that's an increase of 19% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at NZ$2.1m.

In comparison with other companies in the industry with market capitalizations ranging from NZ$1.8b to NZ$5.7b, the reported median CEO total compensation was NZ$5.2m. This suggests that Ross Taylor is paid more than the median for the industry. What's more, Ross Taylor holds NZ$6.6m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | NZ$2.1m | NZ$1.9m | 26% |

| Other | NZ$6.2m | NZ$5.1m | 74% |

| Total Compensation | NZ$8.3m | NZ$7.0m | 100% |

Talking in terms of the industry, salary represented approximately 57% of total compensation out of all the companies we analyzed, while other remuneration made up 43% of the pie. Fletcher Building sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Fletcher Building Limited's Growth

Fletcher Building Limited's earnings per share (EPS) grew 24% per year over the last three years. It achieved revenue growth of 4.7% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Fletcher Building Limited Been A Good Investment?

Fletcher Building Limited has served shareholders reasonably well, with a total return of 23% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 1 warning sign for Fletcher Building that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:FBU

Fletcher Building

Manufactures and distributes building products in New Zealand, Australia, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor