Advertisement

- Norway

- /

- Marine and Shipping

- /

- OB:WAWI

Here's What To Make Of Wallenius Wilhelmsen's (OB:WAWI) Returns On Capital

To find a multi-bagger stock, what are the underlying trends we should look for in a business? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Although, when we looked at Wallenius Wilhelmsen (OB:WAWI), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What is it?

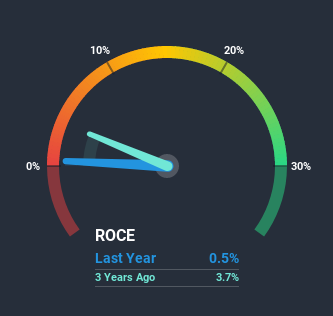

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Wallenius Wilhelmsen is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0046 = US$30m ÷ (US$7.5b - US$1.0b) (Based on the trailing twelve months to September 2020).

So, Wallenius Wilhelmsen has an ROCE of 0.5%. Ultimately, that's a low return and it under-performs the Shipping industry average of 5.3%.

Check out our latest analysis for Wallenius Wilhelmsen

In the above chart we have measured Wallenius Wilhelmsen's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Wallenius Wilhelmsen.

What Can We Tell From Wallenius Wilhelmsen's ROCE Trend?

On the surface, the trend of ROCE at Wallenius Wilhelmsen doesn't inspire confidence. Around five years ago the returns on capital were 3.5%, but since then they've fallen to 0.5%. And considering revenue has dropped while employing more capital, we'd be cautious. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

In Conclusion...

In summary, we're somewhat concerned by Wallenius Wilhelmsen's diminishing returns on increasing amounts of capital. Investors haven't taken kindly to these developments, since the stock has declined 31% from where it was five years ago. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

Wallenius Wilhelmsen does come with some risks though, we found 2 warning signs in our investment analysis, and 1 of those is concerning...

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you decide to trade Wallenius Wilhelmsen, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wallenius Wilhelmsen might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About OB:WAWI

Wallenius Wilhelmsen

Engages in the logistics and transportation business worldwide.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor