Stock Analysis

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Napatech A/S (OB:NAPA) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Napatech

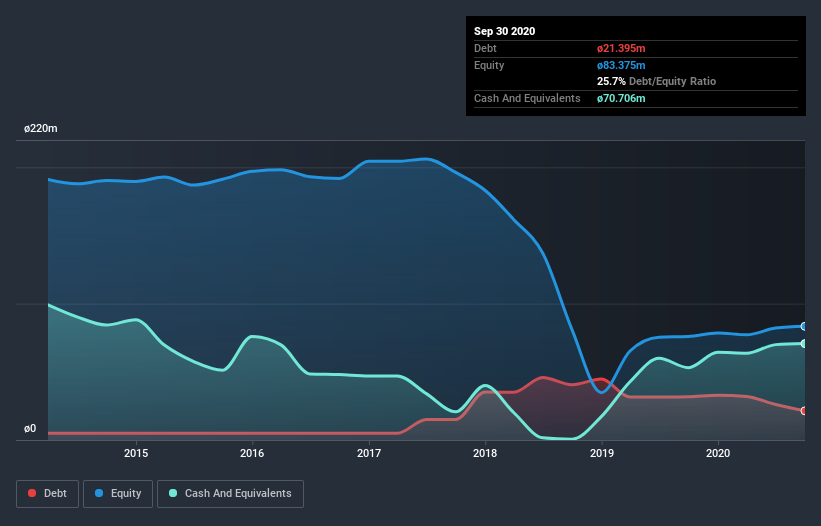

How Much Debt Does Napatech Carry?

As you can see below, Napatech had kr.21.4m of debt at September 2020, down from kr.31.8m a year prior. But it also has kr.70.7m in cash to offset that, meaning it has kr.49.3m net cash.

How Healthy Is Napatech's Balance Sheet?

The latest balance sheet data shows that Napatech had liabilities of kr.45.6m due within a year, and liabilities of kr.20.4m falling due after that. Offsetting these obligations, it had cash of kr.70.7m as well as receivables valued at kr.20.4m due within 12 months. So it actually has kr.25.1m more liquid assets than total liabilities.

This short term liquidity is a sign that Napatech could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Napatech has more cash than debt is arguably a good indication that it can manage its debt safely.

Unfortunately, Napatech's EBIT flopped 13% over the last four quarters. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Napatech can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Napatech has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, Napatech actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Napatech has net cash of kr.49.3m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of kr.34m, being 218% of its EBIT. So we don't have any problem with Napatech's use of debt. Over time, share prices tend to follow earnings per share, so if you're interested in Napatech, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Napatech, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether Napatech is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:NAPA

Napatech

Offers reconfigurable computing solutions for the networking and cybersecurity applications worldwide.

High growth potential with adequate balance sheet.