Advertisement

Is Kitron's €100 Million Defence Win and Upgraded Outlook Altering the Investment Case for Kitron (OB:KIT)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Kitron recently reported strong third-quarter and nine-month earnings, raised its full-year revenue and operating profit guidance, and secured a €100 million order from a Defence/Aerospace client, with deliveries scheduled through 2026.

- This combination of robust financial results, an improved outlook, and substantial new business reflects growing demand in Kitron’s Defence/Aerospace segment and signals increased market confidence.

- To understand the impact of this sizeable Defence/Aerospace order, we’ll explore how it influences Kitron’s overall investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Kitron Investment Narrative Recap

Kitron’s story right now centers on belief in its ability to capture sustained demand in the Defence and Aerospace sector, efficiently scale operations, and manage material costs without eroding margins. The giant €100 million Defence/Aerospace order and recent raised guidance enhance momentum behind the primary short-term catalyst, order backlog growth, while the most pressing risk remains margin pressure due to heavy exposure to lower-margin defense contracts and high input costs.

The most relevant recent announcement is Kitron’s upward revision of its full-year earnings guidance, which directly links to surging Defence/Aerospace demand, just as seen in the recent €100 million order win. This bolsters the argument for further revenue growth, but it also sharpens the focus on how efficiently Kitron can translate this new business into long-term, sustainable profitability given sector headwinds.

But, on the other hand, while investors may be drawn by order growth, the persistent risk of margin pressure is something every shareholder should...

Read the full narrative on Kitron (it's free!)

Kitron's outlook anticipates €1.0 billion in revenue and €71.4 million in earnings by 2028. This requires 16.5% annual revenue growth and a €42.7 million increase in earnings from the current €28.7 million.

Uncover how Kitron's forecasts yield a NOK69.26 fair value, a 8% downside to its current price.

Exploring Other Perspectives

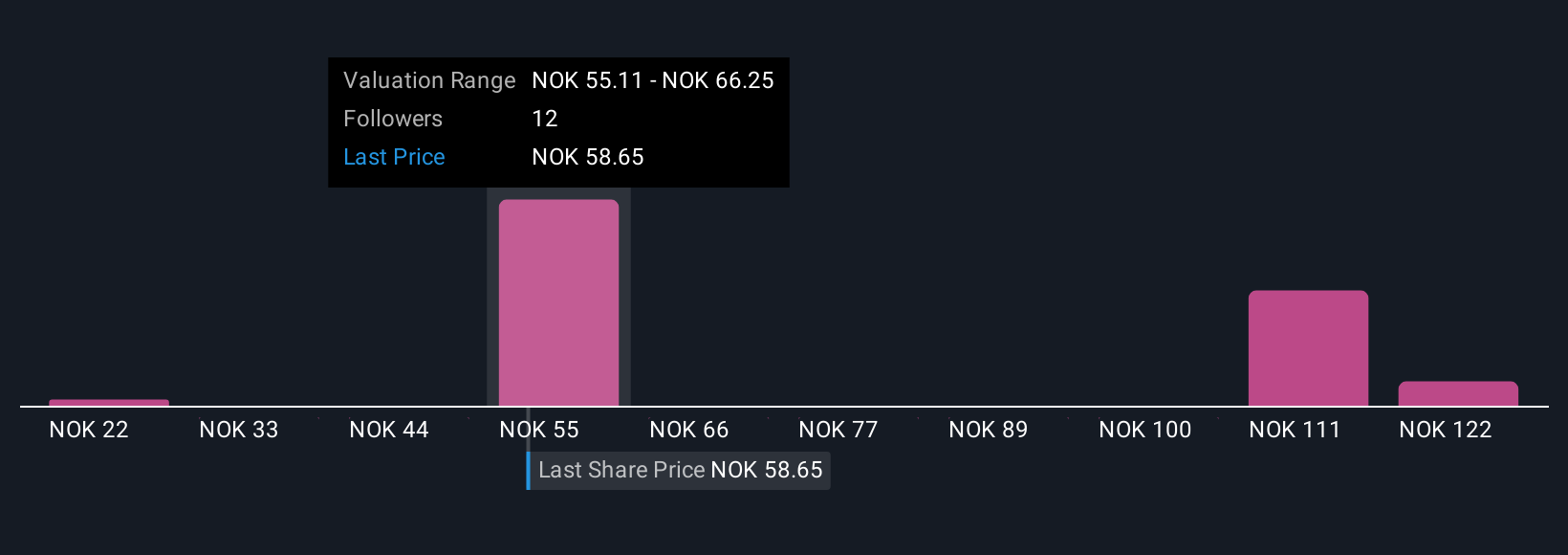

Seven members of the Simply Wall St Community estimate Kitron’s fair value anywhere from NOK21.67 to NOK133.12 per share. With margin pressures linked to defense contracts on investors’ minds, see how these differing outlooks might impact your view of Kitron’s future.

Explore 7 other fair value estimates on Kitron - why the stock might be worth less than half the current price!

Build Your Own Kitron Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kitron research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Kitron research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kitron's overall financial health at a glance.

No Opportunity In Kitron?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kitron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:KIT

Kitron

Operates as an electronics manufacturing services provider in Norway, Sweden, Denmark, Lithuania, Germany, Poland, the Czech Republic, India, China, Malaysia, and the United States.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor