Discover 3 Stocks Including EuroGroup Laminations That May Be Trading Below Estimated Value

Reviewed by Simply Wall St

As global markets experience broad-based gains with U.S. indexes approaching record highs, investors are navigating a landscape marked by strong labor market reports and geopolitical uncertainties. In such an environment, identifying stocks that may be trading below their estimated value can offer potential opportunities for those looking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| HangzhouS MedTech (SHSE:688581) | CN¥62.11 | CN¥124.14 | 50% |

| NBT Bancorp (NasdaqGS:NBTB) | US$50.08 | US$99.93 | 49.9% |

| Truecaller (OM:TRUE B) | SEK47.98 | SEK95.84 | 49.9% |

| Nordic Waterproofing Holding (OM:NWG) | SEK172.40 | SEK344.25 | 49.9% |

| Kitron (OB:KIT) | NOK31.18 | NOK62.32 | 50% |

| Power Root Berhad (KLSE:PWROOT) | MYR1.46 | MYR2.92 | 50% |

| Intermedical Care and Lab Hospital (SET:IMH) | THB4.94 | THB9.86 | 49.9% |

| Neosperience (BIT:NSP) | €0.57 | €1.14 | 50% |

| BATM Advanced Communications (LSE:BVC) | £0.188 | £0.38 | 50% |

| Audinate Group (ASX:AD8) | A$8.79 | A$17.54 | 49.9% |

Below we spotlight a couple of our favorites from our exclusive screener.

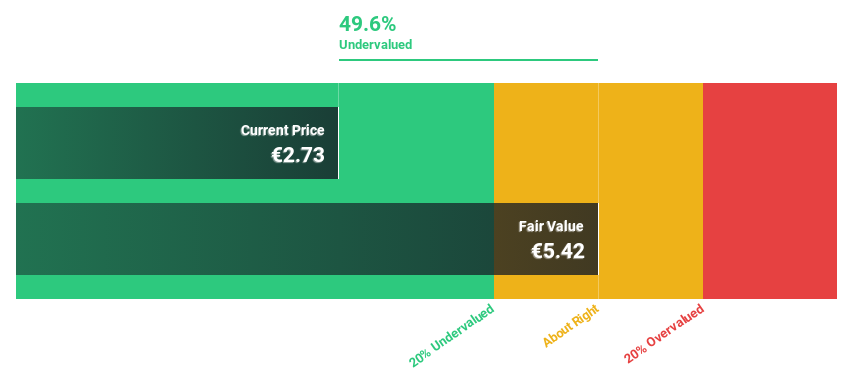

EuroGroup Laminations (BIT:EGLA)

Overview: EuroGroup Laminations S.p.A. designs, produces, and distributes motor cores for electric motors and generators across multiple regions including Europe, the Middle East, Africa, North America, Asia, and China with a market cap of €446.35 million.

Operations: The company's revenue is primarily derived from two segments: Industrial, contributing €311.06 million, and EV & Automotive, accounting for €529.81 million.

Estimated Discount To Fair Value: 49.5%

EuroGroup Laminations is trading at €2.74, significantly below its estimated fair value of €5.43, suggesting it may be undervalued based on cash flows. Despite a volatile share price recently, the company is expected to experience strong earnings growth of 43% annually over the next three years, outpacing the Italian market's growth rate. However, recent financial results show a decline in net income from €27.41 million to €16.86 million year-over-year, indicating potential challenges ahead.

- Our growth report here indicates EuroGroup Laminations may be poised for an improving outlook.

- Click here to discover the nuances of EuroGroup Laminations with our detailed financial health report.

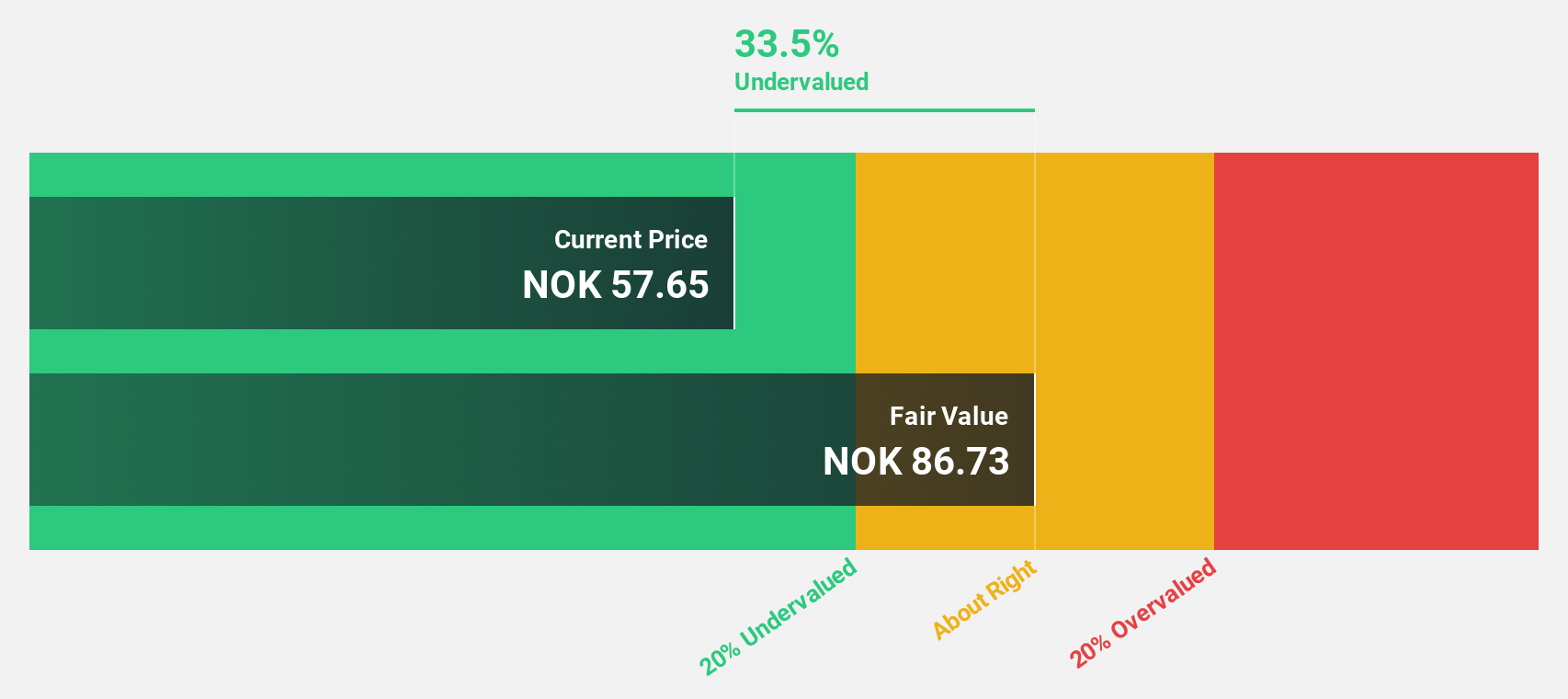

Kitron (OB:KIT)

Overview: Kitron ASA is an electronics manufacturing services company operating in Norway, Sweden, Denmark, Lithuania, Germany, Poland, the Czech Republic, India, China, Malaysia and the United States with a market cap of NOK6.20 billion.

Operations: The company generates revenue of €685.70 million from its Electronics Manufacturing Services (EMS) segment.

Estimated Discount To Fair Value: 50%

Kitron is trading at NOK31.18, significantly below its estimated fair value of NOK62.32, highlighting potential undervaluation based on cash flows. Despite a decline in recent earnings, with Q3 net income falling to €6.1 million from €9.7 million year-over-year, the company forecasts earnings growth of 15.5% annually, outpacing the Norwegian market's 9.2%. However, Kitron carries a high level of debt and revised its full-year revenue guidance downward recently.

- Our comprehensive growth report raises the possibility that Kitron is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of Kitron.

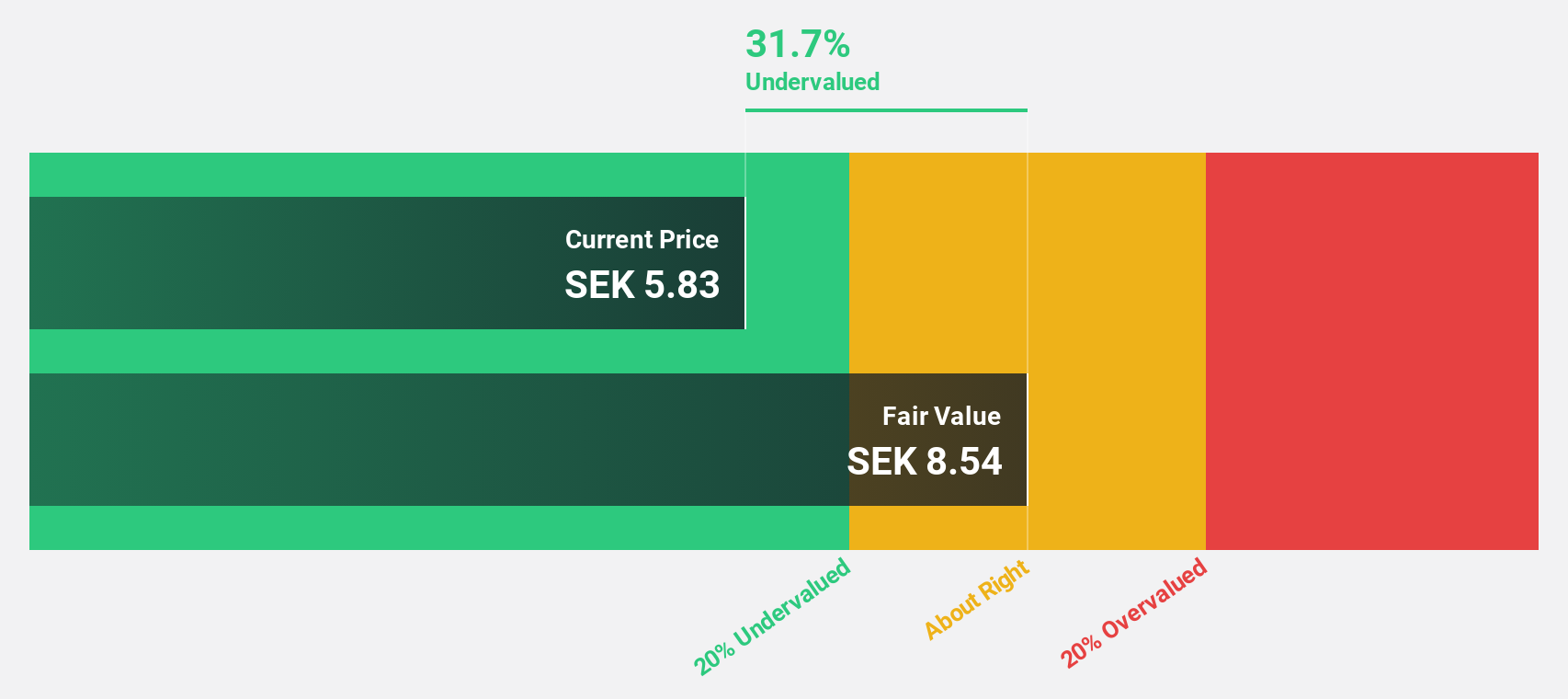

Nyab (OM:NYAB)

Overview: Nyab AB (publ) operates in Finland and Sweden, offering engineering, construction, and maintenance services for energy, infrastructure, and industrial projects in both public and private sectors, with a market cap of approximately SEK3.73 billion.

Operations: The company generates revenue from its heavy construction segment, which amounts to €314.33 million.

Estimated Discount To Fair Value: 48.3%

NYAB is trading at SEK5.45, significantly below its estimated fair value of SEK10.55, suggesting potential undervaluation based on cash flows. Despite a decrease in profit margins from last year, NYAB's earnings are projected to grow by 26.8% annually, surpassing the Swedish market's growth rate of 15.1%. Recent challenges include a withdrawn tramway contract award decision and executive changes with the appointment of a new CFO starting December 2024.

- The analysis detailed in our Nyab growth report hints at robust future financial performance.

- Click to explore a detailed breakdown of our findings in Nyab's balance sheet health report.

Taking Advantage

- Discover the full array of 926 Undervalued Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kitron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:KIT

Kitron

Operates as an electronics manufacturing services company in Norway, Sweden, Denmark, Lithuania, Germany, Poland, the Czech Republic, India, China, Malaysia, and the United States.

Undervalued with excellent balance sheet.