Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Komplett ASA (OB:KOMPL) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does Komplett Carry?

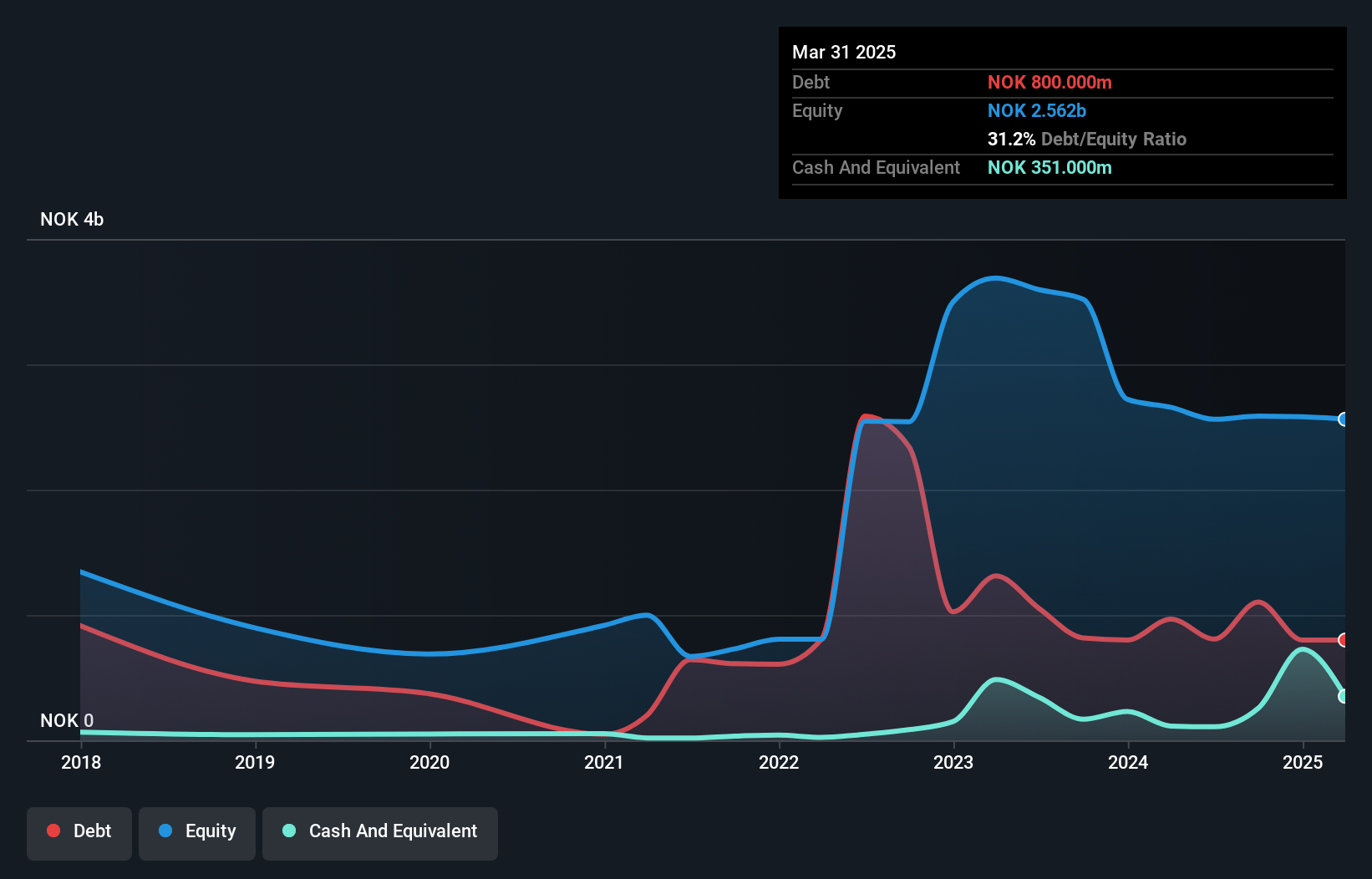

You can click the graphic below for the historical numbers, but it shows that Komplett had kr800.0m of debt in March 2025, down from kr967.0m, one year before. However, because it has a cash reserve of kr351.0m, its net debt is less, at about kr449.0m.

How Strong Is Komplett's Balance Sheet?

According to the last reported balance sheet, Komplett had liabilities of kr2.97b due within 12 months, and liabilities of kr1.67b due beyond 12 months. Offsetting this, it had kr351.0m in cash and kr734.0m in receivables that were due within 12 months. So it has liabilities totalling kr3.56b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the kr2.10b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Komplett would likely require a major re-capitalisation if it had to pay its creditors today. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Komplett can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Check out our latest analysis for Komplett

In the last year Komplett's revenue was pretty flat, and it made a negative EBIT. While that's not too bad, we'd prefer see growth.

Caveat Emptor

Importantly, Komplett had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost kr78m at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. It's fair to say the loss of kr197m didn't encourage us either; we'd like to see a profit. In the meantime, we consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example - Komplett has 1 warning sign we think you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Komplett might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:KOMPL

Komplett

Operates as an online retailer of electronics products in Norway, Sweden, and Denmark.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|36.2% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|18.7% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|22.0% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|5.0% overvalued

TO

Community Contributor