Advertisement

- Norway

- /

- Energy Services

- /

- OB:TGS

New Gulf of America Contract and Strong Results Could Be a Game Changer for TGS (OB:TGS)

Simply Wall St

Reviewed by Sasha Jovanovic

- TGS ASA recently reported third quarter 2025 results, announcing net income of US$62 million on sales of US$424.4 million, and confirmed a quarterly dividend of NOK1.56 per share payable on November 13, 2025, following prior shareholder approval.

- In addition, TGS received an OBN acquisition contract for a 4D monitor survey in the Gulf of America, a deal not previously included in its contracted backlog, highlighting ongoing project momentum.

- To assess the impact on TGS's investment outlook, we will consider how improved profitability alongside the new Gulf of America contract informs future earnings potential.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

TGS Investment Narrative Recap

To be a TGS shareholder, you need to believe that future global energy demand will drive exploration activity and that the company’s seismic data and digitalization initiatives can convert that demand into reliable earnings growth. While the recently announced OBN contract in the Gulf of America builds project momentum, the company’s revenue remains highly sensitive to oil price volatility and concentrated client exposure, so this news does not materially reduce short-term earnings risks or the potential for revenue swings.

The standout announcement here is TGS’s new 4D monitor survey contract for the Gulf of America, which was not previously included in the company’s backlog. This addition increases near-term project activity, providing some cushion against weak Q2 sales, yet the impact on the major risk, revenue volatility from top-client dependence and oil market swings, remains to be seen.

However, investors should be aware that despite recent contract wins, the real test could arise if a key client delays or cancels a major project and ...

Read the full narrative on TGS (it's free!)

TGS is expected to reach $1.5 billion in revenue and $226.2 million in earnings by 2028. This outlook assumes a 5.7% annual revenue decline and forecasts an earnings increase of $201.2 million from the current level of $25.0 million.

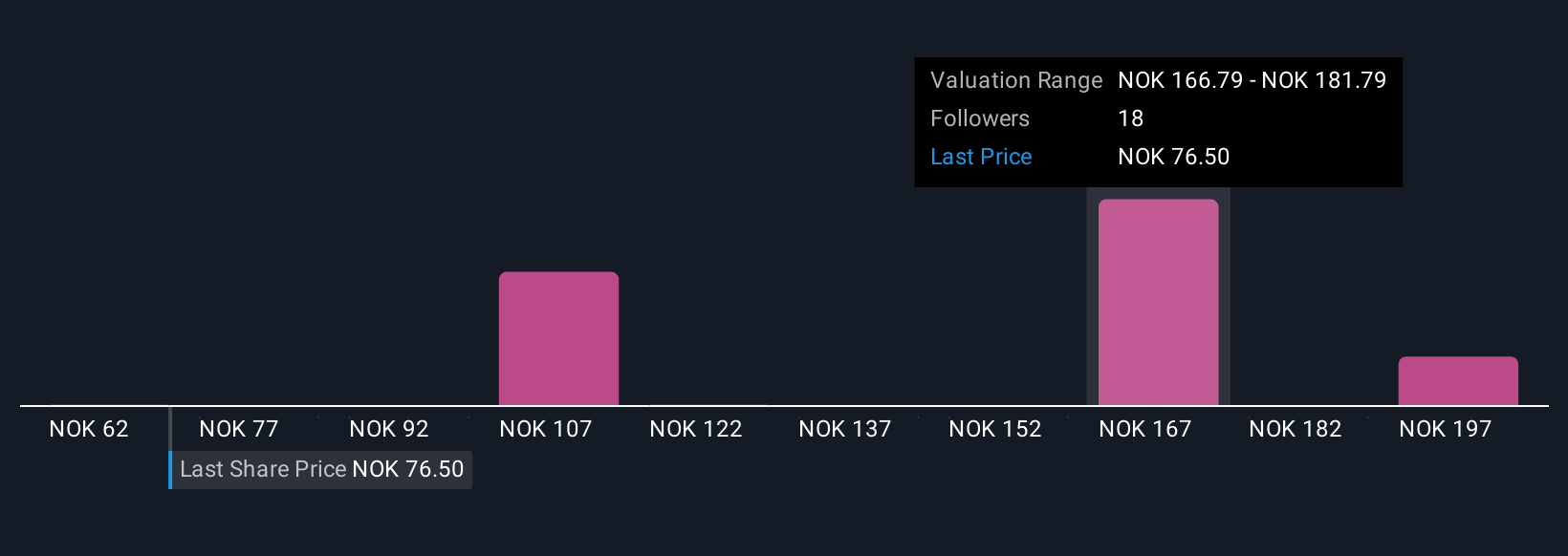

Uncover how TGS' forecasts yield a NOK124.93 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Six community fair value estimates for TGS range from NOK61.77 to NOK255.89, with viewpoints spanning nearly a fourfold difference. While many see upside, keep in mind that renewed contract momentum can be offset by persistent revenue volatility, so consider several perspectives before making a judgment.

Explore 6 other fair value estimates on TGS - why the stock might be worth 28% less than the current price!

Build Your Own TGS Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TGS research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free TGS research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TGS' overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've found 24 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TGS might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:TGS

TGS

Provides geoscience data services to the oil and gas industry in Norway and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor