Advertisement

- Norway

- /

- Energy Services

- /

- OB:SHLF

Shelf Drilling's (OB:SHLF) Shareholders Should Assess Earnings With Caution

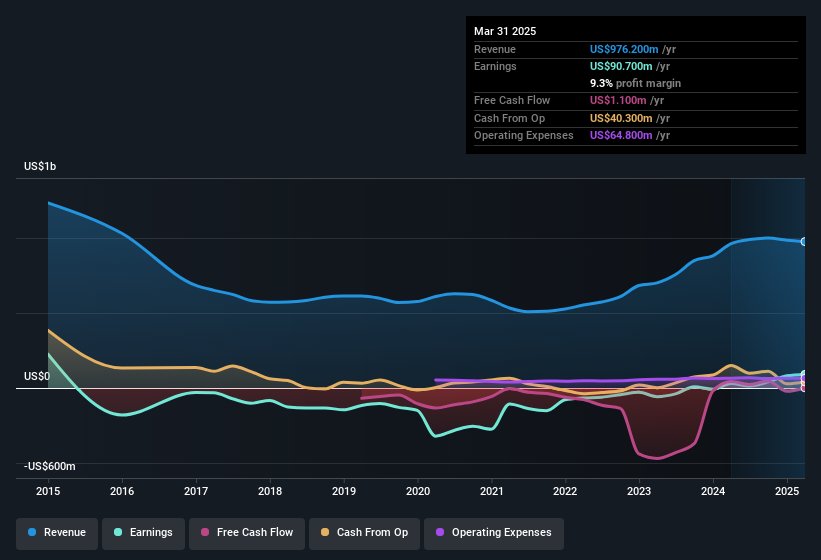

Shelf Drilling, Ltd.'s (OB:SHLF) stock rose after it released a robust earnings report. While the headline numbers were strong, we found some underlying problems once we started looking at what drove earnings.

We've discovered 5 warning signs about Shelf Drilling. View them for free.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, Shelf Drilling issued 20% more new shares over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Shelf Drilling's historical EPS growth by clicking on this link.

A Look At The Impact Of Shelf Drilling's Dilution On Its Earnings Per Share (EPS)

Three years ago, Shelf Drilling lost money. The good news is that profit was up 200% in the last twelve months. On the other hand, earnings per share are only up 162% over the same period. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, earnings per share growth should beget share price growth. So Shelf Drilling shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Finally, we should also consider the fact that unusual items boosted Shelf Drilling's net profit by US$59m over the last year. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. We can see that Shelf Drilling's positive unusual items were quite significant relative to its profit in the year to March 2025. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Shelf Drilling's Profit Performance

To sum it all up, Shelf Drilling got a nice boost to profit from unusual items; without that, its statutory results would have looked worse. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. For the reasons mentioned above, we think that a perfunctory glance at Shelf Drilling's statutory profits might make it look better than it really is on an underlying level. So while earnings quality is important, it's equally important to consider the risks facing Shelf Drilling at this point in time. For example, we've found that Shelf Drilling has 5 warning signs (2 are potentially serious!) that deserve your attention before going any further with your analysis.

Our examination of Shelf Drilling has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:SHLF

Shelf Drilling

Operates as a shallow water offshore drilling contractor in the Middle East, North Africa, the Mediterranean, Southeast Asia, India, West Africa, and the North Sea.

Proven track record with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor