Advertisement

- Norway

- /

- Energy Services

- /

- OB:AKSO

kr12.80: That's What Analysts Think Aker Solutions ASA (OB:AKSO) Is Worth After Its Latest Results

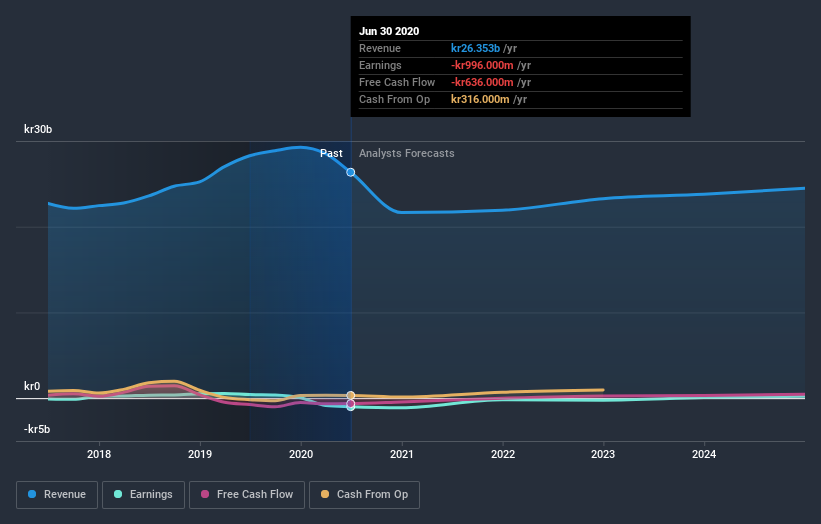

Aker Solutions ASA (OB:AKSO) just released its latest second-quarter results and things are looking bullish. Revenues and losses per share both beat expectations, with revenues of kr5.4b leading estimates by 6.8%. Statutory losses were somewhat smaller thanthe analysts expected, coming in at kr0.65 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Aker Solutions

Taking into account the latest results, the current consensus, from the eleven analysts covering Aker Solutions, is for revenues of kr21.7b in 2020, which would reflect an uncomfortable 18% reduction in Aker Solutions' sales over the past 12 months. Losses are expected to increase substantially, hitting kr4.15 per share. Yet prior to the latest earnings, the analysts had been forecasting revenues of kr20.6b and losses of kr3.82 per share in 2020. Overall it looks as though the analysts were a bit mixed on the latest consensus updates. Although there was a nice uplift to revenue, the consensus also made a to its losses per share forecasts.

It will come as no surprise that expanding losses caused the consensus price target to fall 6.0% to kr12.80with the analysts implicitly ranking ongoing losses as a greater concern than growing revenues. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Aker Solutions analyst has a price target of kr35.00 per share, while the most pessimistic values it at kr8.00. With such a wide range in price targets, analysts are almost certainly betting on widely divergent outcomes in the underlying business. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. Compare this against analyst estimates for companies in the wider industry, which suggest that revenues (in aggregate) are expected to decline 0.5% next year. So it's pretty clear that Aker Solutions sales are expected to decline at a faster rate than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. They also upgraded their revenue estimates, with sales apparently performing well, although revenues are expected to lag the wider industry this year. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Aker Solutions' future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Aker Solutions. Long-term earnings power is much more important than next year's profits. We have forecasts for Aker Solutions going out to 2024, and you can see them free on our platform here.

You still need to take note of risks, for example - Aker Solutions has 2 warning signs (and 1 which doesn't sit too well with us) we think you should know about.

When trading Aker Solutions or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About OB:AKSO

Aker Solutions

Provides solutions, products, systems, and services to the oil and gas industry in Norway, the United States, Brazil, the United Kingdom, Malaysia, Angola, Brunei, Canada, India, and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor