Advertisement

- Norway

- /

- Professional Services

- /

- OB:ZAL

This Is Why Zalaris ASA's (OB:ZAL) CEO Compensation Looks Appropriate

Key Insights

- Zalaris' Annual General Meeting to take place on 19th of June

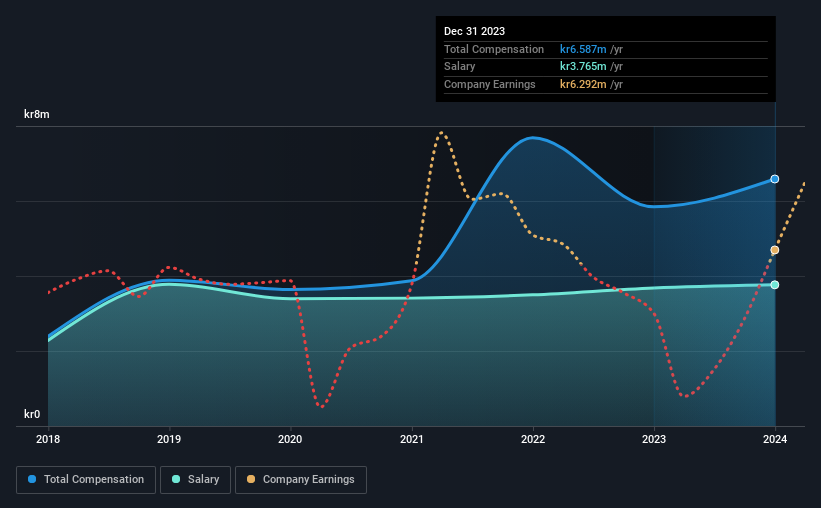

- CEO Hans-Petter Mellerud's total compensation includes salary of kr3.77m

- The total compensation is similar to the average for the industry

- Over the past three years, Zalaris' EPS fell by 17% and over the past three years, the total shareholder return was 32%

CEO Hans-Petter Mellerud has done a decent job of delivering relatively good performance at Zalaris ASA (OB:ZAL) recently. As shareholders go into the upcoming AGM on 19th of June, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. Here is our take on why we think the CEO compensation looks appropriate.

See our latest analysis for Zalaris

How Does Total Compensation For Hans-Petter Mellerud Compare With Other Companies In The Industry?

According to our data, Zalaris ASA has a market capitalization of kr1.7b, and paid its CEO total annual compensation worth kr6.6m over the year to December 2023. Notably, that's an increase of 13% over the year before. Notably, the salary which is kr3.77m, represents a considerable chunk of the total compensation being paid.

In comparison with other companies in the Norway Professional Services industry with market capitalizations ranging from kr1.1b to kr4.3b, the reported median CEO total compensation was kr5.3m. From this we gather that Hans-Petter Mellerud is paid around the median for CEOs in the industry. What's more, Hans-Petter Mellerud holds kr221m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr3.8m | kr3.7m | 57% |

| Other | kr2.8m | kr2.2m | 43% |

| Total Compensation | kr6.6m | kr5.8m | 100% |

Speaking on an industry level, nearly 65% of total compensation represents salary, while the remainder of 35% is other remuneration. It's interesting to note that Zalaris allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Zalaris ASA's Growth

Over the last three years, Zalaris ASA has shrunk its earnings per share by 17% per year. It achieved revenue growth of 26% over the last year.

The reduction in EPS, over three years, is arguably concerning. But on the other hand, revenue growth is strong, suggesting a brighter future. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Zalaris ASA Been A Good Investment?

With a total shareholder return of 32% over three years, Zalaris ASA shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

Some shareholders will be pleased by the relatively good results, however, the results could still be improved. Despite robust revenue growth, until EPS growth improves, shareholders may be hesitant to increase CEO pay by too much.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 2 warning signs for Zalaris (of which 1 can't be ignored!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Zalaris might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:ZAL

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor