Advertisement

SpareBank 1 Nordmøre (OB:SNOR) Margin Surge Challenges Defensive Banking Narrative

Simply Wall St

Reviewed by Simply Wall St

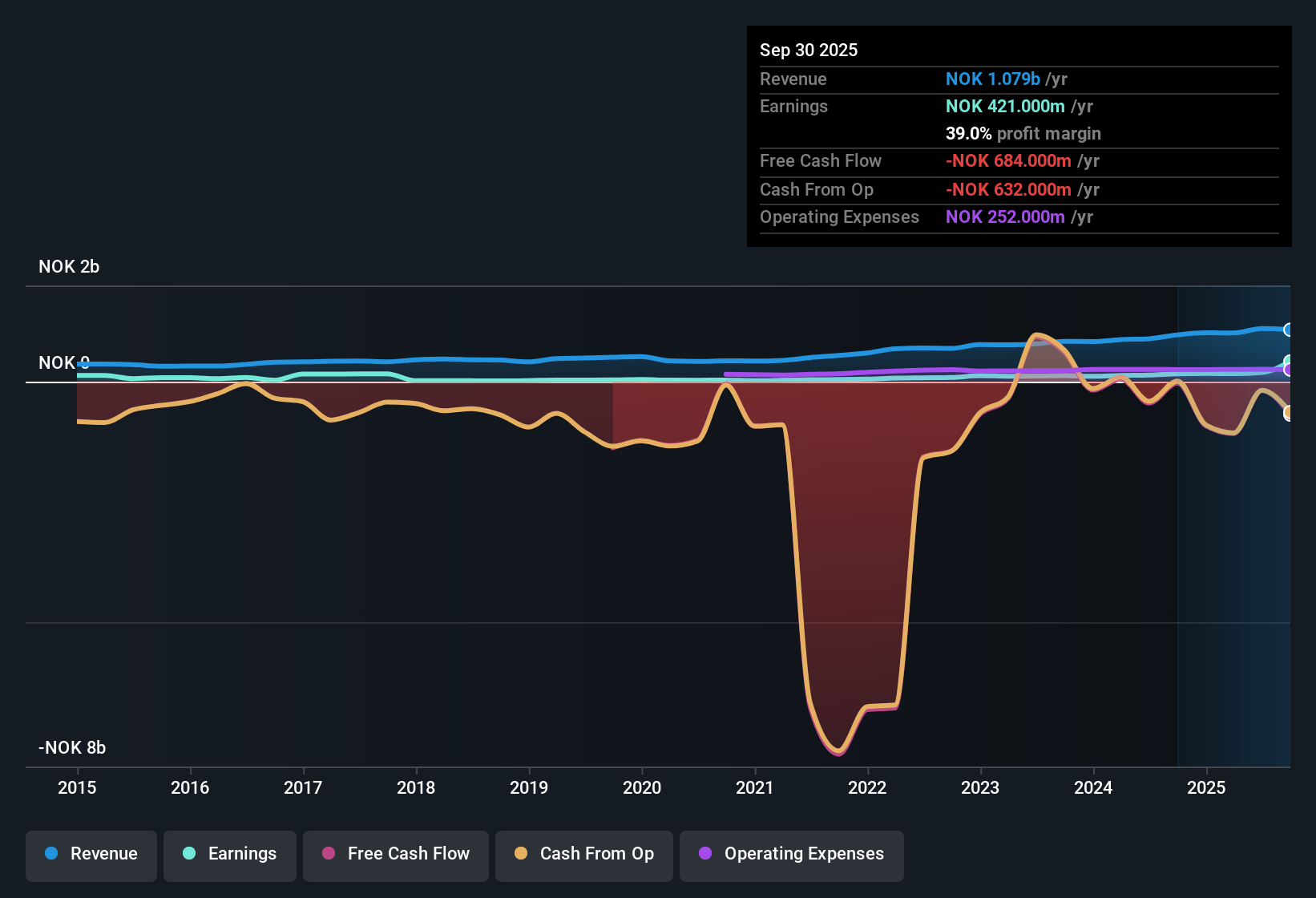

SpareBank 1 Nordmøre (OB:SNOR) reported a net profit margin of 39%, up from 16.9% a year ago. Annual earnings increased by 156.7%, which is significantly above its 5-year average growth of 39.9%. Despite expectations for revenue to decline by 0.5% annually over the next three years and forward earnings growth to slow to 2.5% per year compared to the Norwegian market’s 16.7%, the bank’s shares now trade at a considerable discount—just 3.6x earnings versus the peer average of 14.9x, and well below the NOK522.14 estimated fair value. With high-quality earnings and a history of profit growth, SpareBank 1 Nordmøre’s strong margin expansion and discounted share price give the results notable weight for investors.

See our full analysis for SpareBank 1 Nordmøre.The next section compares the latest performance numbers with the widely followed narratives from the Simply Wall St community to see how well the story holds up.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Expansion Signals Defensive Strength

- The net profit margin rose sharply to 39% from last year's 16.9%, nearly tripling profitability in twelve months.

- What is striking is that, despite only moderate optimism in local sentiment, this margin leap strongly supports the view that SpareBank 1 Nordmøre stands out as a defensive regional banking pick in Norway.

- While sector narratives focus on safety and predictability, this surge demonstrates the bank is not just “stable” but also capturing meaningful upside from its business model.

- The margin performance outpaces peers’ averages and provides factual backing for investors looking for resilience in a low-growth environment.

Forecasts Foreshadow Slower Growth Versus Market

- Forward annual earnings growth is projected at 2.5%, trailing well behind the broader Norwegian market’s 16.7% expected pace.

- What is surprising in light of this outlook is that, while positive sector sentiment exists around prudent management and a steady dividend, most retail and investor discussions acknowledge that upside is capped by these softer growth projections.

- Investors appreciate the reliability, but limited growth keeps the case from turning outright bullish, especially compared to higher-growth banks.

- The current forecast reinforces the idea that SpareBank 1 Nordmøre’s appeal hinges more on stability and income than aggressive expansion.

Deep Value Discount Widens to Peers

- Shares now trade at a price-to-earnings ratio of 3.6x, well below both the peer average (14.9x) and the Norwegian banking sector (10.7x) while the NOK169.52 share price sits at less than one-third the calculated DCF fair value of NOK522.14.

- Consensus narrative notes that, although the investment community expects only modest performance ahead, the unusually wide valuation gap may offer material support for price as long as margins and low-risk characteristics persist.

- The sector’s stated preference is for safety and downside protection, and this discount could draw further interest from investors looking for “bargain” defensive names.

- Yet, with revenue expected to decline and growth forecasts subdued, upside re-rating likely depends on the bank sustaining or improving these profitability metrics.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on SpareBank 1 Nordmøre's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite a standout profit margin, SpareBank 1 Nordmøre faces weak revenue forecasts and is expected to grow earnings much more slowly than the broader market.

If you want exposure to companies set for stronger, more consistent gains, now is the time to discover stable growth stocks screener (2091 results) that are outperforming on stable long-term growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:SNOR

SpareBank 1 Nordmøre

Provides various banking products and services in Norway.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor