Advertisement

Assessing Sparebanken Norge (OB:SBNOR) Valuation Following Strong Earnings Growth and Insider Buying

Simply Wall St

Reviewed by Kshitija Bhandaru

Sparebanken Norge (OB:SBNOR) is drawing attention after reporting impressive earnings growth, accompanied by a wave of insider share purchases. This combination often signals rising management confidence and can spark fresh investor interest.

See our latest analysis for Sparebanken Norge.

Momentum has been quietly building for Sparebanken Norge, with a solid stretch of earnings growth and management’s increased stake helping to support sentiment. The stock’s latest share price remains resilient at 173.7 NOK. Its one-year total shareholder return of 0.48% reflects gradual long-term gains amid a steady operating backdrop.

If the combination of strong financials and enthusiastic insiders piques your curiosity, now is the perfect time to discover fast growing stocks with high insider ownership

But with robust results and insider optimism already on display, investors are left to wonder if Sparebanken Norge is still trading below its true worth, or if the market has already priced in its future growth potential.

Price-to-Earnings of 9x: Is it justified?

At a price-to-earnings (P/E) ratio of 9x, Sparebanken Norge’s current valuation sits below both the broader Norwegian market and its direct banking peers, hinting at possible undervaluation relative to profit generation. With a last close price of 173.7 NOK, the multiple positions the stock as attractively priced for investors focused on earnings as a key driver.

The price-to-earnings ratio shows how much investors are willing to pay for each unit of a company’s earnings. In banking, this metric is crucial because it helps compare profitability and market expectations across similar institutions.

This low P/E suggests the market may be underpricing Sparebanken Norge’s underlying earnings power and future prospects, especially as its profit growth outpaces the sector. Compared to the Norwegian Banks industry average of 10.7x, SBNOR’s ratio stands out as strong relative value. In relation to the estimated fair price-to-earnings ratio of 13.9x, there is even greater headroom for rerating if expectations rise.

Explore the SWS fair ratio for Sparebanken Norge

Result: Price-to-Earnings of 9x (UNDERVALUED)

However, continued market optimism may hinge on maintaining above-average earnings growth. Any deterioration in sector sentiment could quickly challenge the current valuation story.

Find out about the key risks to this Sparebanken Norge narrative.

Another View: What About Discounted Cash Flow?

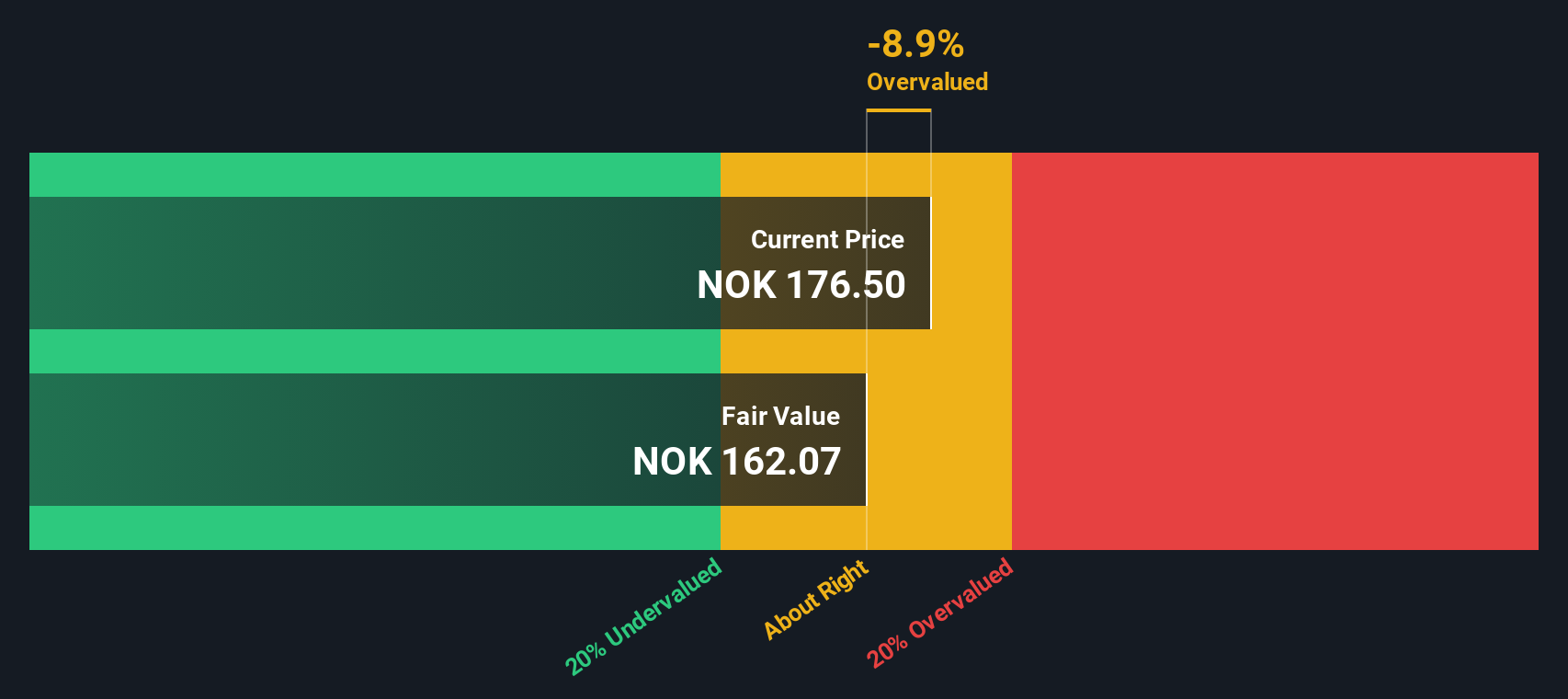

While the price-to-earnings ratio points to Sparebanken Norge being undervalued, our DCF model presents a more cautious picture. According to this approach, the stock is actually trading above its fair value estimate of 163.29 NOK. Does this suggest the market is running ahead of fundamentals, or is there more upside in store?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sparebanken Norge for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sparebanken Norge Narrative

If you want to reach your own verdict or prefer hands-on research, you can craft your own perspective on Sparebanken Norge in just a few minutes, so why not Do it your way

A great starting point for your Sparebanken Norge research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock tomorrow’s potential by targeting unique opportunities using the Simply Wall Street Screener. If you wait, you could miss some of the market’s most exciting moves.

- Get ahead of the curve and spot major breakthroughs by checking out these 24 AI penny stocks as they reshape industries with artificial intelligence.

- Boost your passive income strategy by reviewing these 19 dividend stocks with yields > 3% that offer consistently strong yields above 3%.

- Tap into future finance trends by exploring these 78 cryptocurrency and blockchain stocks leading the charge in blockchain innovation and digital assets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:SBNOR

Sparebanken Norge

Sparebanken Vest, a financial services company, provides banking and financing services in the counties of Vestland and Rogaland, Norway.

Reasonable growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor