- Netherlands

- /

- Machinery

- /

- ENXTAM:ENVI

Insider-Owned Growth Leaders On Euronext Amsterdam In May 2024

Reviewed by Simply Wall St

As global markets show signs of stabilization with easing inflation concerns, the Euronext Amsterdam stands out with its unique offerings. This article will explore three growth companies in the Netherlands that not only demonstrate robust potential but also boast high insider ownership, aligning leadership interests closely with shareholder value in these promising times.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Envipco Holding (ENXTAM:ENVI) | 15.1% | 69.2% |

| Ebusco Holding (ENXTAM:EBUS) | 31.4% | 115.2% |

| MotorK (ENXTAM:MTRK) | 35.8% | 105.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 66.1% |

| PostNL (ENXTAM:PNL) | 30.8% | 24.3% |

Below we spotlight a couple of our favorites from our exclusive screener.

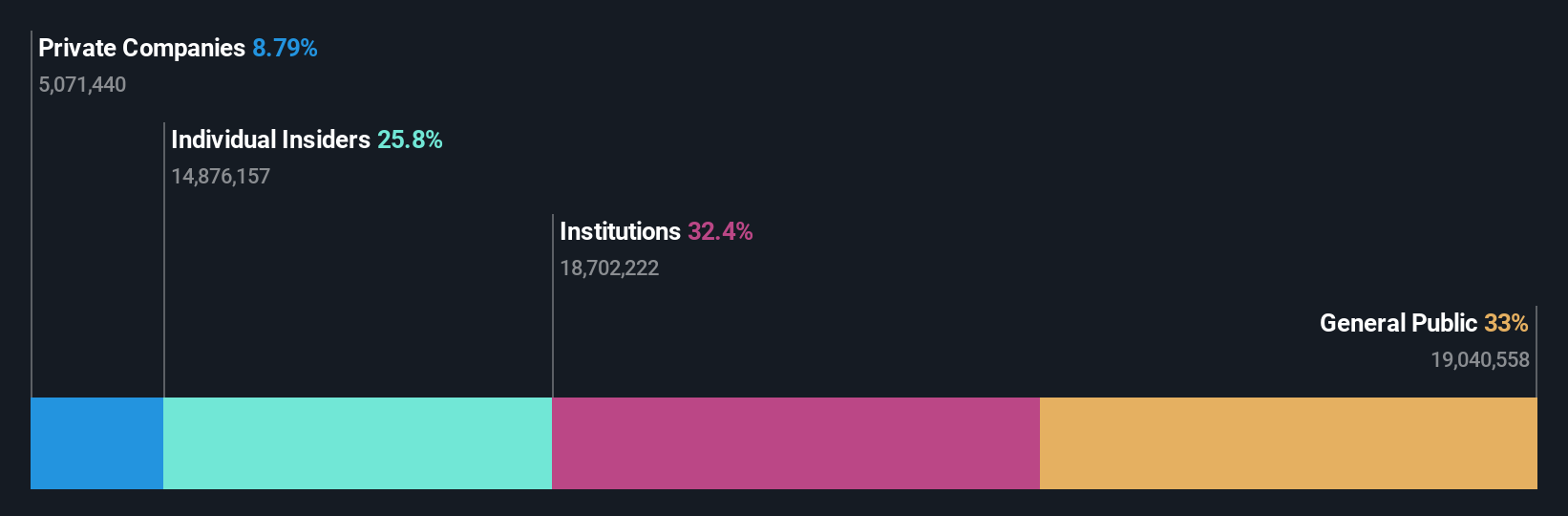

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★★

Overview: Envipco Holding N.V. specializes in designing, developing, manufacturing, and selling or leasing reverse vending machines for recycling used beverage containers, primarily serving markets in the Netherlands, North America, and Europe with a market capitalization of €360.56 million.

Operations: The company generates its revenue by designing, developing, manufacturing, and selling or leasing reverse vending machines for recycling used beverage containers across the Netherlands, North America, and Europe.

Insider Ownership: 15.1%

Earnings Growth Forecast: 69.2% p.a.

Envipco Holding N.V. stands out in the Netherlands for its robust growth prospects, with revenue expected to increase by 34.4% per year and earnings by 69.2% annually, significantly outpacing the broader Dutch market's growth rates of 9.2% and 15.9%, respectively. Despite recent high volatility in its share price and shareholder dilution over the past year, Envipco has become profitable this year and is trading at a considerable discount to its estimated fair value, enhancing its appeal among growth-focused investors with high insider ownership interests.

- Unlock comprehensive insights into our analysis of Envipco Holding stock in this growth report.

- Our comprehensive valuation report raises the possibility that Envipco Holding is priced lower than what may be justified by its financials.

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc operates as a provider of software-as-a-service solutions tailored for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union, with a market capitalization of approximately €263.96 million.

Operations: The company generates revenue primarily through its software and programming segment, which amounted to €42.94 million.

Insider Ownership: 35.8%

Earnings Growth Forecast: 105.8% p.a.

MotorK, while navigating recent executive changes and a net loss reported for the previous fiscal year, shows promising growth trajectories in the Netherlands. The company's revenue is expected to grow by 24% annually, outperforming the Dutch market average of 9.2%. Despite shareholder dilution last year, MotorK's forecast to become profitable within three years aligns with its high revenue growth expectations. However, challenges remain as it still projects a net loss in the coming years.

- Click here to discover the nuances of MotorK with our detailed analytical future growth report.

- The valuation report we've compiled suggests that MotorK's current price could be inflated.

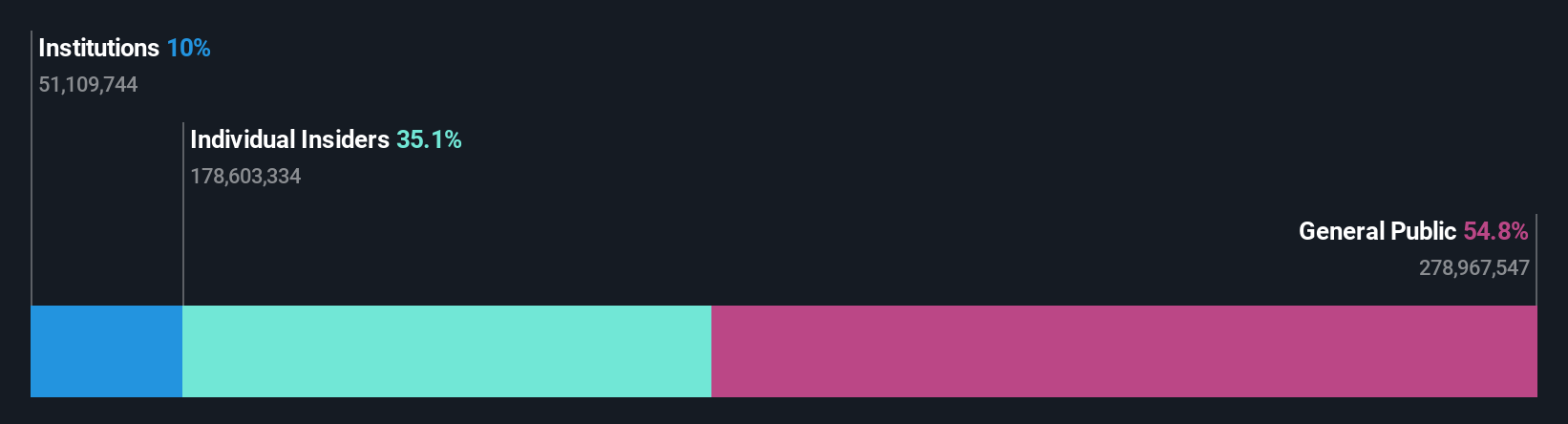

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, other parts of Europe, and internationally, with a market capitalization of approximately €0.62 billion.

Operations: The company generates revenue primarily from its Packages and Mail in The Netherlands segments, amounting to €2.25 billion and €1.35 billion respectively.

Insider Ownership: 30.8%

Earnings Growth Forecast: 24.3% p.a.

PostNL, a company based in the Netherlands, is experiencing robust earnings growth, forecasted at 24.3% per year, outpacing the Dutch market average. Despite this strong growth projection and a return to profitability this year, challenges include a high debt level and slower revenue growth at 3.4% annually compared to the market's 9.2%. Recent financials indicate a net loss in Q1 2024 with sales declining from previous periods, highlighting volatility in its financial performance amidst its recovery trajectory.

- Click to explore a detailed breakdown of our findings in PostNL's earnings growth report.

- Our valuation report here indicates PostNL may be undervalued.

Make It Happen

- Unlock more gems! Our Fast Growing Euronext Amsterdam Companies With High Insider Ownership screener has unearthed 2 more companies for you to explore.Click here to unveil our expertly curated list of 5 Fast Growing Euronext Amsterdam Companies With High Insider Ownership.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Envipco Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:ENVI

Envipco Holding

Designs, develops, manufactures, assembles, markets, sells, leases, and services reverse vending machines (RVM) to collect and process used beverage containers primarily in the Netherlands, North America, and rest of Europe.

High growth potential with adequate balance sheet.