Stock Analysis

- Netherlands

- /

- Software

- /

- ENXTAM:MTRK

High Insider Ownership Growth Stocks On Euronext Amsterdam May 2024

Reviewed by Simply Wall St

As global markets continue to navigate through fluctuating economic indicators and monetary policies, the Euronext Amsterdam remains a focal point for investors looking for growth opportunities. In this context, companies with high insider ownership can be particularly appealing, as this often signals confidence from those closest to the company's operations and future prospects.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Envipco Holding (ENXTAM:ENVI) | 15.1% | 67.8% |

| Ebusco Holding (ENXTAM:EBUS) | 31.4% | 115.2% |

| MotorK (ENXTAM:MTRK) | 35.8% | 105.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 66.1% |

| PostNL (ENXTAM:PNL) | 30.8% | 24.3% |

Here's a peek at a few of the choices from the screener.

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Envipco Holding N.V. specializes in designing, developing, manufacturing, and selling or leasing reverse vending machines for recycling used beverage containers, operating mainly in the Netherlands, North America, and Europe with a market capitalization of approximately €360.56 million.

Operations: The company generates revenue through the design, development, manufacture, and sale or lease of reverse vending machines in the Netherlands, North America, and Europe.

Insider Ownership: 15.1%

Envipco Holding N.V. has recently shown a remarkable recovery, transitioning from a net loss to profitability with its latest annual earnings reporting an increase in sales to €87.58 million and net income of €1.42 million. Despite this progress and a forecasted revenue growth rate of 33.4% per year, the company's share price remains highly volatile, and shareholder dilution occurred over the past year due to a follow-on equity offering raising NOK 300 million. Additionally, while Envipco's earnings are expected to grow significantly at 67.8% annually, there is no recent insider trading data available to gauge current insider confidence directly.

- Click here and access our complete growth analysis report to understand the dynamics of Envipco Holding.

- The valuation report we've compiled suggests that Envipco Holding's current price could be inflated.

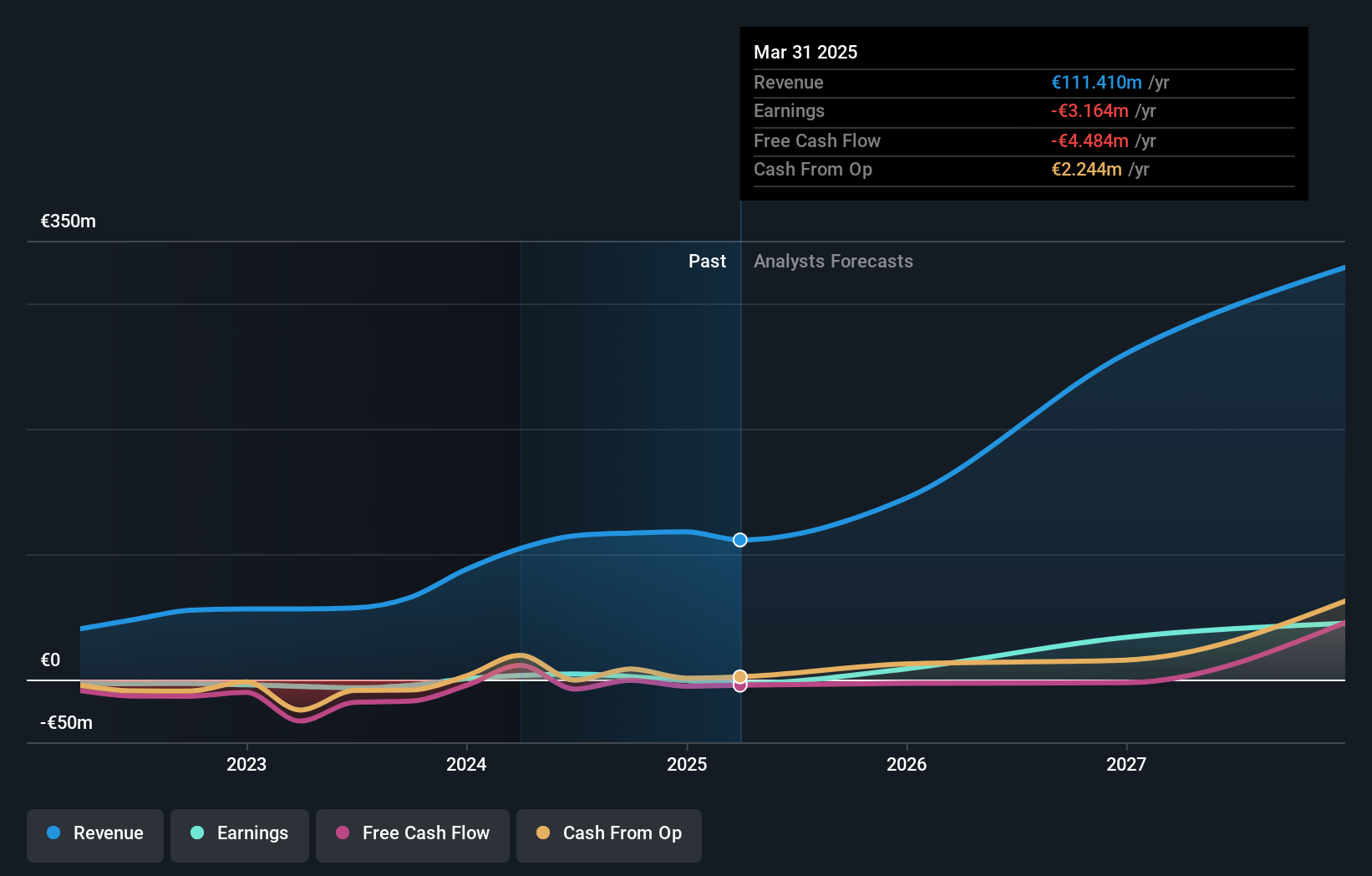

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc operates as a provider of software-as-a-service solutions tailored for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union, with a market capitalization of approximately €270.34 million.

Operations: The company generates revenue primarily through its software and programming segment, totaling €42.94 million.

Insider Ownership: 35.8%

MotorK plc, a growth-oriented company in the Netherlands with high insider ownership, is navigating challenges alongside opportunities. Despite a recent dip in quarterly revenue to €11.25 million and an increase in net loss to €13.25 million for the full year, MotorK forecasts robust annual revenue growth at 24% per year and expects its Committed Annual Recurring Revenues to reach €50 million by fiscal year-end 2024. The company's potential profitability within three years aligns with above-market expectations, although shareholder dilution has occurred over the past year.

- Take a closer look at MotorK's potential here in our earnings growth report.

- Our expertly prepared valuation report MotorK implies its share price may be too high.

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, Europe, and globally, with a market capitalization of approximately €0.63 billion.

Operations: The company's revenue is derived primarily from its Packages and Mail in The Netherlands segments, generating €2.25 billion and €1.35 billion respectively.

Insider Ownership: 30.8%

PostNL, a Dutch company with high insider ownership, has faced challenges recently, reporting a decline in quarterly sales to €763 million and swinging to a net loss of €20 million in Q1 2024. Despite this setback, the company has shown resilience by proposing dividends and maintaining shareholder payouts. Looking ahead, PostNL forecasts normalized EBIT between €80 million and €110 million for 2024. With earnings expected to grow by 24.3% annually over the next three years, PostNL's financial outlook appears promising despite current hurdles and a high level of debt.

- Navigate through the intricacies of PostNL with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report PostNL implies its share price may be lower than expected.

Turning Ideas Into Actions

- Unlock our comprehensive list of 5 Fast Growing Euronext Amsterdam Companies With High Insider Ownership by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether MotorK is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:MTRK

MotorK

Provides software-as-a-service for the automotive retail industry in Italy, Spain, France, Germany, and the Benelux Union.

High growth potential with excellent balance sheet.