- Netherlands

- /

- Machinery

- /

- ENXTAM:ENVI

Euronext Amsterdam Showcases 3 Growth Companies With Up To 35% Insider Ownership

Reviewed by Simply Wall St

Amidst a backdrop of fluctuating global markets and political uncertainties in Europe, the Euronext Amsterdam stands out by showcasing growth companies with significant insider ownership. High insider ownership often signals strong confidence in the company's future prospects, making these stocks particularly interesting in the current economic climate.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| BenevolentAI (ENXTAM:BAI) | 27.8% | 62.8% |

| Envipco Holding (ENXTAM:ENVI) | 15.1% | 68.9% |

| Ebusco Holding (ENXTAM:EBUS) | 34% | 115.2% |

| MotorK (ENXTAM:MTRK) | 35.8% | 105.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 66.1% |

| PostNL (ENXTAM:PNL) | 30.8% | 24.2% |

Below we spotlight a couple of our favorites from our exclusive screener.

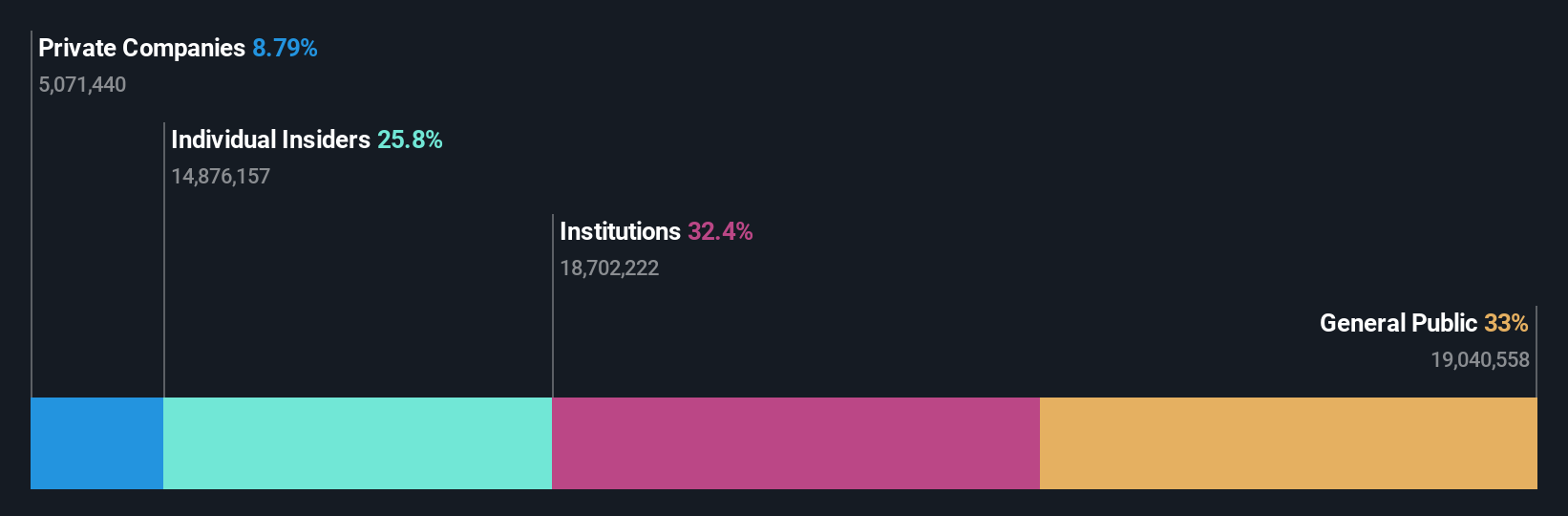

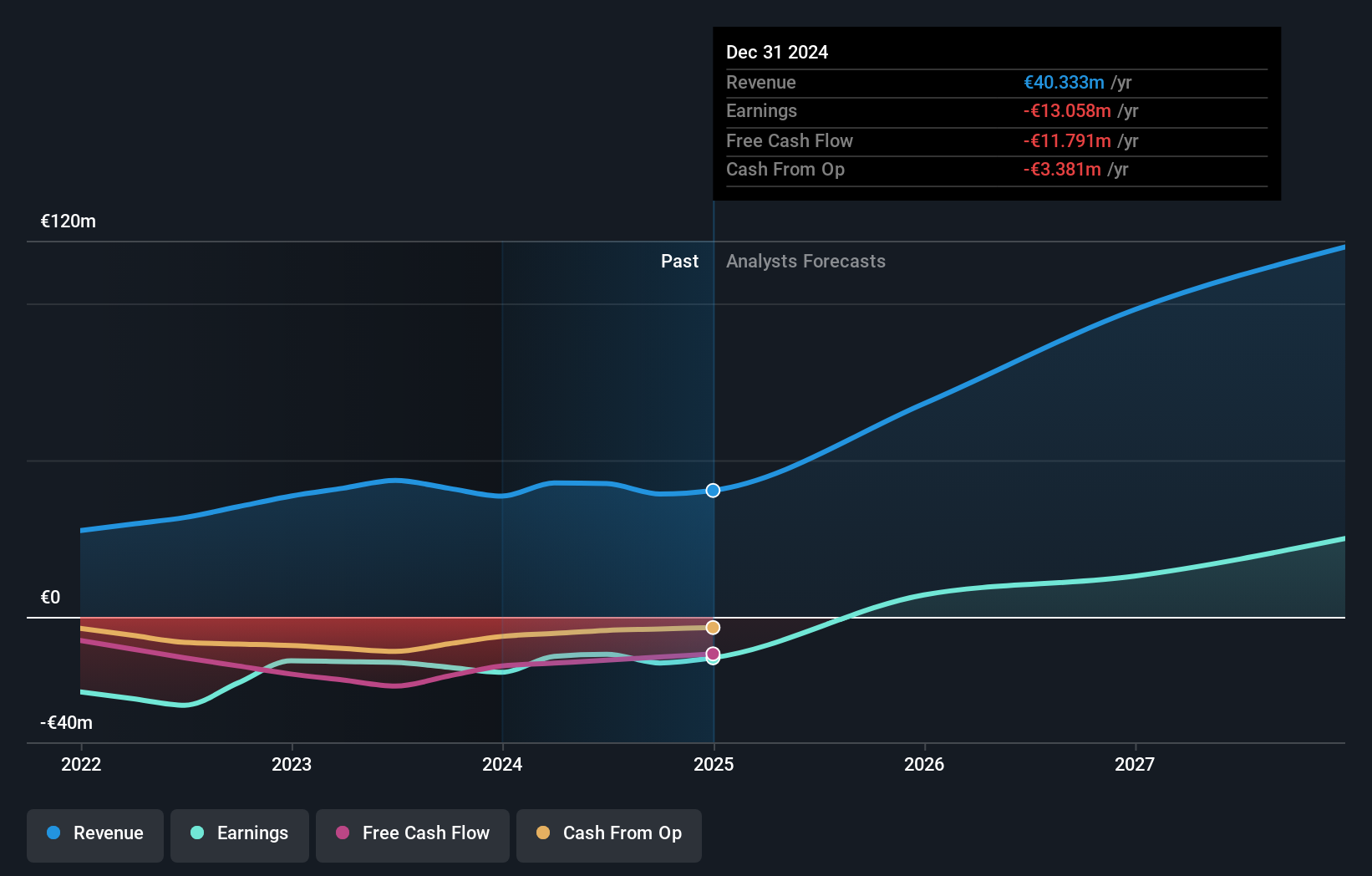

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Envipco Holding N.V. operates primarily in the Netherlands, North America, and Europe, focusing on designing, developing, manufacturing, and selling or leasing reverse vending machines (RVMs) for processing used beverage containers, with a market capitalization of approximately €357.68 million.

Operations: The company generates revenue by designing, developing, manufacturing, and either selling or leasing reverse vending machines mainly across the Netherlands, North America, and Europe.

Insider Ownership: 15.1%

Envipco Holding has demonstrated a strong turnaround, transitioning from a net loss of €2.57 million to a net profit of €0.147 million in the first quarter of 2024, with sales increasing to €27.44 million from €10.41 million year-over-year. Despite its highly volatile share price and recent shareholder dilution, the company is trading at a significant discount to its estimated fair value and is expected to see robust growth in earnings (68.91% per year) and revenue (33.6% per year), outpacing the Dutch market forecasts significantly.

- Click to explore a detailed breakdown of our findings in Envipco Holding's earnings growth report.

- Our valuation report here indicates Envipco Holding may be overvalued.

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc operates as a software-as-a-service provider tailored for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union, with a market capitalization of approximately €268.46 million.

Operations: The company generates its revenue primarily through its software and programming segment, which brought in €42.94 million.

Insider Ownership: 35.8%

MotorK, despite experiencing slight revenue decline in Q1 2024 with EUR 11.25 million compared to EUR 11.43 million the previous year, is poised for substantial growth. The company's revenue and earnings are expected to surge by 24% and 105.85% per year respectively, outperforming the Dutch market significantly. However, recent changes in the board and a past year's shareholder dilution present challenges. MotorK is forecasted to transition from unprofitable to profitable within three years, reflecting potential amidst uncertainties.

- Click here and access our complete growth analysis report to understand the dynamics of MotorK.

- Upon reviewing our latest valuation report, MotorK's share price might be too optimistic.

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, Europe, and globally, with a market capitalization of approximately €0.68 billion.

Operations: The company's revenue is primarily derived from its Packages and Mail in The Netherlands segments, generating €2.25 billion and €1.35 billion respectively.

Insider Ownership: 30.8%

PostNL, while trading at 48.7% below its estimated fair value, shows promise with a high forecast return on equity of 27.3% in three years and earnings expected to grow by 24.2% annually, outpacing the Dutch market's 16.5%. However, its revenue growth lags behind the market expectation at only 3.4% per year and it carries a high debt level. Recent activities include completing a €298.67 million sustainability-linked bond offering, aiming to bolster its financial position amidst an unstable dividend track record and shareholder dilution over the past year.

- Unlock comprehensive insights into our analysis of PostNL stock in this growth report.

- Upon reviewing our latest valuation report, PostNL's share price might be too pessimistic.

Seize The Opportunity

- Click through to start exploring the rest of the 3 Fast Growing Euronext Amsterdam Companies With High Insider Ownership now.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Envipco Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:ENVI

Envipco Holding

Designs, develops, manufactures, assembles, markets, sells, leases, and services reverse vending machines (RVM) to collect and process used beverage containers primarily in the Netherlands, North America, and rest of Europe.

High growth potential with adequate balance sheet.