Advertisement

- Netherlands

- /

- Logistics

- /

- ENXTAM:PNL

3 Stocks Estimated To Be Trading Below Fair Value In January 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the early days of President Trump's administration, U.S. stocks are reaching record highs driven by optimism over potential trade negotiations and AI investments. Amid this buoyant market atmosphere, identifying stocks that are trading below their fair value can present unique opportunities for investors seeking to capitalize on potential mispricings in the market.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Türkiye Sise Ve Cam Fabrikalari (IBSE:SISE) | TRY38.86 | TRY77.57 | 49.9% |

| Fevertree Drinks (AIM:FEVR) | £6.58 | £13.12 | 49.9% |

| Atea (OB:ATEA) | NOK139.40 | NOK278.37 | 49.9% |

| East Side Games Group (TSX:EAGR) | CA$0.57 | CA$1.14 | 50% |

| Kinaxis (TSX:KXS) | CA$170.04 | CA$339.70 | 49.9% |

| J Trust (TSE:8508) | ¥521.00 | ¥1039.92 | 49.9% |

| GemPharmatech (SHSE:688046) | CN¥13.06 | CN¥26.03 | 49.8% |

| IDP Education (ASX:IEL) | A$13.17 | A$26.31 | 50% |

| Allied Blenders and Distillers (NSEI:ABDL) | ₹394.40 | ₹787.12 | 49.9% |

| Cavotec (OM:CCC) | SEK20.00 | SEK39.88 | 49.8% |

Here we highlight a subset of our preferred stocks from the screener.

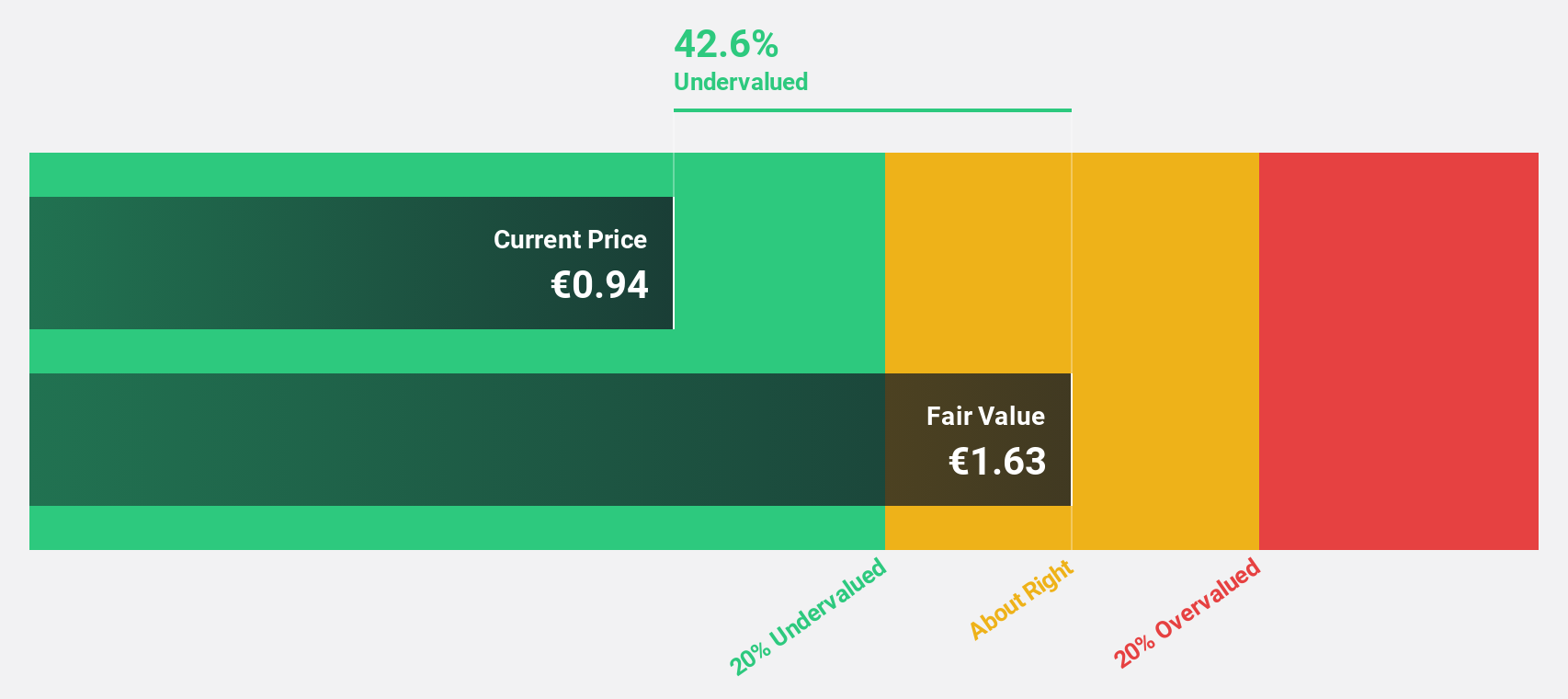

PostNL (ENXTAM:PNL)

Overview: PostNL N.V. offers postal and logistics services to businesses and consumers in the Netherlands, Europe, and internationally, with a market cap of €482.03 million.

Operations: The company's revenue segments include postal and logistics services provided to businesses and consumers across the Netherlands, Europe, and internationally.

Estimated Discount To Fair Value: 47.1%

PostNL is trading at €0.96, significantly below its estimated fair value of €1.82, presenting an undervaluation based on discounted cash flow analysis. Despite a high debt level and a dividend yield of 6.25% not covered by earnings, the company's earnings are forecast to grow substantially at 44.9% annually over the next three years, outpacing the Dutch market's growth rate of 14.5%. Recent guidance anticipates normalized EBIT around €53 million for 2024 amidst past losses.

- The growth report we've compiled suggests that PostNL's future prospects could be on the up.

- Take a closer look at PostNL's balance sheet health here in our report.

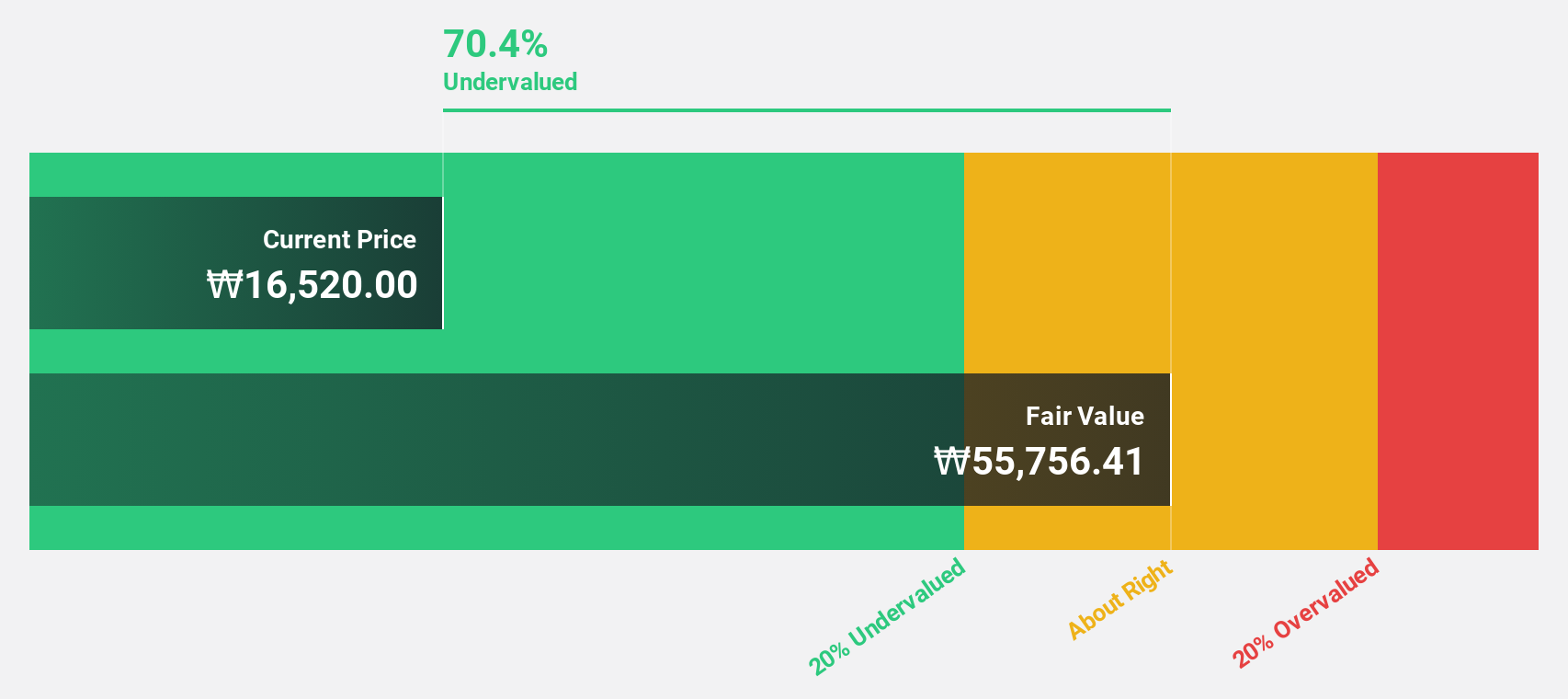

Solum (KOSE:A248070)

Overview: Solum Co., Ltd. is a company that produces and sells power modules, digital tuners, and electronic shelf labels both in South Korea and globally, with a market cap of approximately ₩912.18 billion.

Operations: The company's revenue is derived from its ICT Business, which generated ₩432.21 million, and its Electronic Components Division, contributing ₩1.14 billion.

Estimated Discount To Fair Value: 49.6%

Solum is trading at ₩18,950, significantly below its estimated fair value of ₩37,596.95, highlighting potential undervaluation based on cash flows. Despite a high debt level and declining profit margins from 5.8% to 2.8%, earnings are projected to grow substantially by 50% annually over the next three years, surpassing the Korean market's growth rate of 27.8%. Recent AI-enhanced product innovations in digital signage could enhance revenue streams amid growing retail media networks.

- Our expertly prepared growth report on Solum implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of Solum.

Shenzhen Xinyichang Technology (SHSE:688383)

Overview: Shenzhen Xinyichang Technology Co., Ltd. specializes in the research, development, production, and sale of intelligent manufacturing equipment for industries such as LED, capacitor, semiconductor, and lithium battery in China with a market cap of CN¥4.43 billion.

Operations: Shenzhen Xinyichang Technology generates revenue through the development and sale of advanced manufacturing equipment tailored for the LED, capacitor, semiconductor, and lithium battery sectors within China.

Estimated Discount To Fair Value: 24.5%

Shenzhen Xinyichang Technology is trading at CNY 43.48, significantly below its estimated fair value of CNY 57.6, indicating potential undervaluation based on cash flows. Despite high debt levels, the company has shown strong earnings growth of 40.2% over the past year and is expected to continue growing earnings by 47.6% annually, outpacing the Chinese market's projected growth rate of 25%. Recent share buybacks reflect management's confidence in future performance.

- Our earnings growth report unveils the potential for significant increases in Shenzhen Xinyichang Technology's future results.

- Get an in-depth perspective on Shenzhen Xinyichang Technology's balance sheet by reading our health report here.

Next Steps

- Access the full spectrum of 899 Undervalued Stocks Based On Cash Flows by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:PNL

PostNL

Provides postal and logistics services to businesses and consumers in the Netherlands, rest of Europe, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor