Advertisement

- Netherlands

- /

- Semiconductors

- /

- ENXTAM:ASML

ASML Holding (AMS:ASML) Knows How To Allocate Capital Effectively

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, the ROCE of ASML Holding (AMS:ASML) looks great, so lets see what the trend can tell us.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on ASML Holding is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

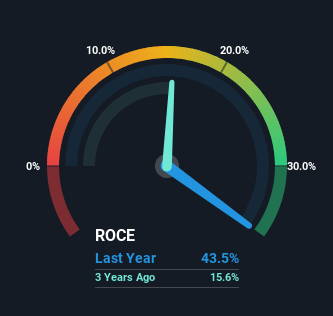

0.44 = €7.9b ÷ (€35b - €17b) (Based on the trailing twelve months to April 2023).

So, ASML Holding has an ROCE of 44%. In absolute terms that's a great return and it's even better than the Semiconductor industry average of 15%.

Check out our latest analysis for ASML Holding

In the above chart we have measured ASML Holding's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for ASML Holding.

SWOT Analysis for ASML Holding

Strength

- Earnings growth over the past year exceeded the industry.

- Debt is not viewed as a risk.

Weakness

- Dividend is low compared to the top 25% of dividend payers in the Semiconductor market.

- Expensive based on P/E ratio and estimated fair value.

Opportunity

- Annual earnings are forecast to grow faster than the Dutch market.

Threat

- Revenue is forecast to grow slower than 20% per year.

What The Trend Of ROCE Can Tell Us

ASML Holding has not disappointed with their ROCE growth. The figures show that over the last five years, ROCE has grown 194% whilst employing roughly the same amount of capital. So our take on this is that the business has increased efficiencies to generate these higher returns, all the while not needing to make any additional investments. It's worth looking deeper into this though because while it's great that the business is more efficient, it might also mean that going forward the areas to invest internally for the organic growth are lacking.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Effectively this means that suppliers or short-term creditors are now funding 48% of the business, which is more than it was five years ago. And with current liabilities at those levels, that's pretty high.

What We Can Learn From ASML Holding's ROCE

In summary, we're delighted to see that ASML Holding has been able to increase efficiencies and earn higher rates of return on the same amount of capital. Since the stock has returned a staggering 311% to shareholders over the last five years, it looks like investors are recognizing these changes. Therefore, we think it would be worth your time to check if these trends are going to continue.

On the other side of ROCE, we have to consider valuation. That's why we have a FREE intrinsic value estimation on our platform that is definitely worth checking out.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTAM:ASML

ASML Holding

Provides lithography solutions for the development, production, marketing, sales, upgrading, and servicing of advanced semiconductor equipment systems.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor