Advertisement

- Netherlands

- /

- Semiconductors

- /

- ENXTAM:ASML

ASML (ENXTAM:ASML): Assessing Valuation After Strong Share Price Gains

Simply Wall St

Reviewed by Simply Wall St

ASML Holding (ENXTAM:ASML) shares have delivered strong returns over the past year, gaining 40%. Investors have watched the semiconductor equipment giant's performance closely, given ongoing demand shifts in the industry and its steady fundamentals.

See our latest analysis for ASML Holding.

ASML Holding’s share price has climbed an impressive 31.5% in 2024, with momentum accelerating in recent months as optimism grows around semiconductor demand and the company’s unique market position. Its long-term performance stands out too, with a 3-year total shareholder return nearing 94% and a 5-year total return close to 200%, underscoring robust growth potential and continued investor confidence.

If the strength in semiconductor equipment stocks has piqued your interest, this could be the perfect moment to explore more opportunities in the high-growth tech and AI space using our curated screener: See the full list for free.

But with ASML’s share price near record highs and much of its future growth already reflected in its valuation, investors face a critical question: is there still room for upside or is the market fully pricing in its prospects?

Most Popular Narrative: 9% Undervalued

According to Investingwilly’s narrative, the fair value for ASML is €1,000, which stands above the last close price of €907.4. This gap highlights the belief that the market has not fully recognized the company’s true earnings power and growth trajectory. Let’s take a look at what’s driving this perspective.

ASML is the only company in the world producing EUV lithography tools. These machines are essential for making the world’s most powerful semiconductors. This gives ASML a near monopoly in a fast-growing market driven by AI, 5G, and high-performance computing.

Want to unpack what’s fueling this high price target? The narrative hinges on breakthrough technology access, powerful recurring revenues, and projections that hint at a scale few rivals can match. If you’re curious about which future metrics and cash flows set ASML apart, the full narrative walks through the assumptions powering this compelling upside story.

Result: Fair Value of €1,000 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain, including macroeconomic pressures and new export restrictions to China. Both factors could hinder ASML’s near-term growth trajectory.

Find out about the key risks to this ASML Holding narrative.

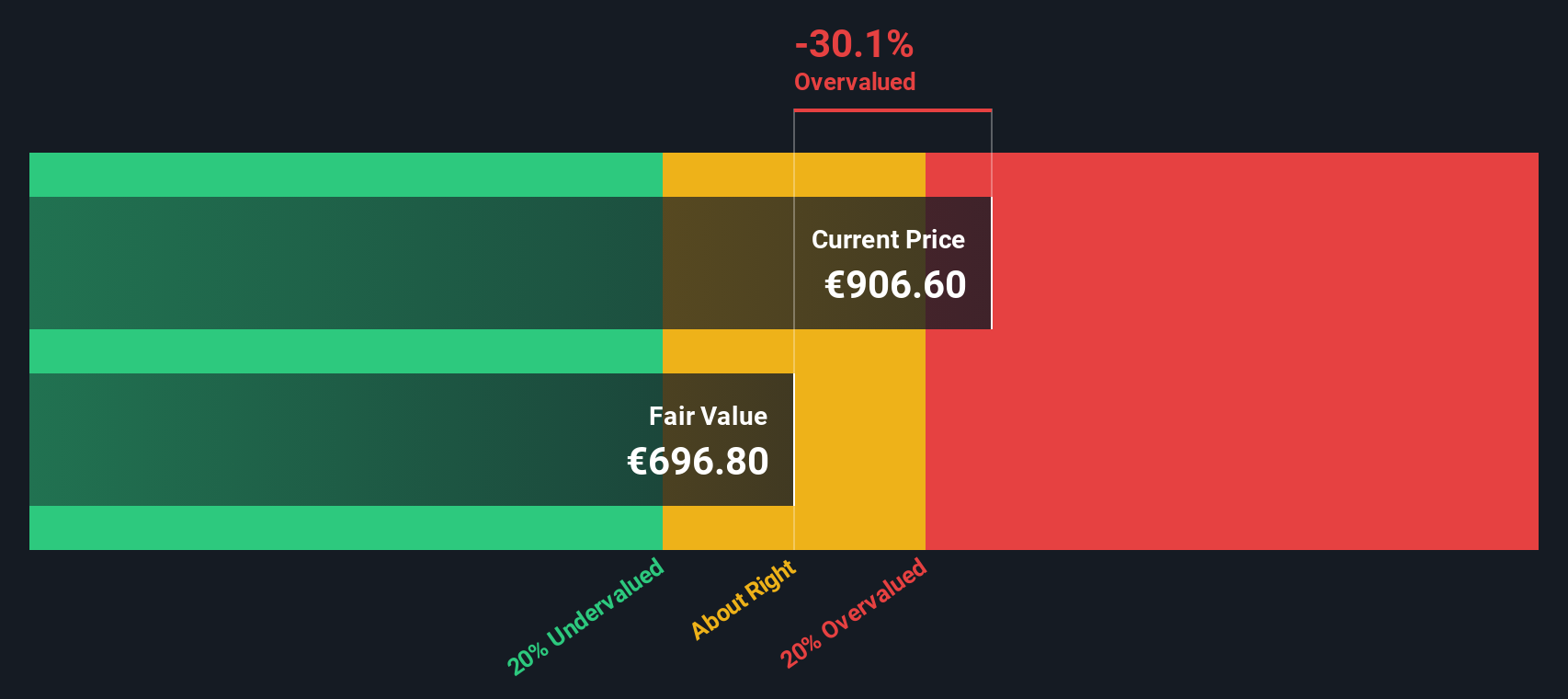

Another View: A Different Take on Value

Not everyone shares the optimism found in user narratives. According to our DCF model, ASML is actually trading above its estimated fair value of €645.7 per share. This suggests the market may be overly enthusiastic about the company’s future cash flows. Does this highlight a risk, or could the market be on to something others are missing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASML Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ASML Holding Narrative

If you’d like to challenge these viewpoints or prefer to analyze the numbers yourself, you can easily craft your own narrative in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding ASML Holding.

Looking for More Investment Ideas?

Don’t let the next winning opportunity slip by. Level up your strategy with handpicked stock ideas tailored to today’s trends and tomorrow’s growth stories.

- Uncover value with these 870 undervalued stocks based on cash flows that may be under the radar but have strong fundamentals and attractive pricing for savvy investors.

- Boost your passive income by checking out these 21 dividend stocks with yields > 3% with higher yields and the financial strength to support consistent payouts.

- Seize the future by reviewing these 28 quantum computing stocks pushing boundaries in advanced computing technology and innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:ASML

ASML Holding

Provides lithography solutions for the development, production, marketing, sales, upgrading, and servicing of advanced semiconductor equipment systems.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor