Advertisement

- Malaysia

- /

- Wireless Telecom

- /

- KLSE:AXIATA

Insufficient Growth At Axiata Group Berhad (KLSE:AXIATA) Hampers Share Price

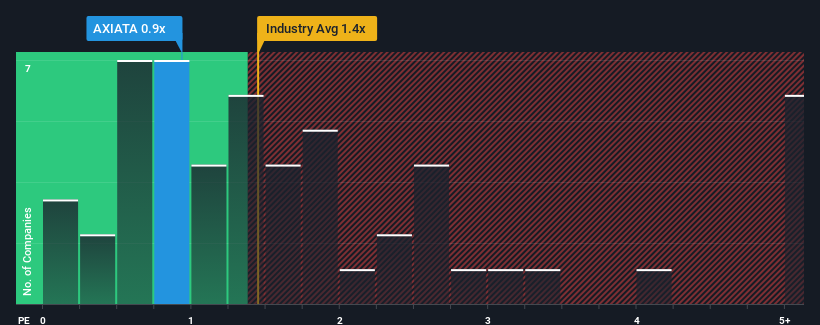

When you see that almost half of the companies in the Wireless Telecom industry in Malaysia have price-to-sales ratios (or "P/S") above 1.9x, Axiata Group Berhad (KLSE:AXIATA) looks to be giving off some buy signals with its 0.9x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for Axiata Group Berhad

How Has Axiata Group Berhad Performed Recently?

Recent revenue growth for Axiata Group Berhad has been in line with the industry. One possibility is that the P/S ratio is low because investors think this modest revenue performance may begin to slide. Those who are bullish on Axiata Group Berhad will be hoping that this isn't the case.

Want the full picture on analyst estimates for the company? Then our free report on Axiata Group Berhad will help you uncover what's on the horizon.How Is Axiata Group Berhad's Revenue Growth Trending?

In order to justify its P/S ratio, Axiata Group Berhad would need to produce sluggish growth that's trailing the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 8.0%. However, this wasn't enough as the latest three year period has seen an unpleasant 8.0% overall drop in revenue. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 3.3% per year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 6.2% each year, which is noticeably more attractive.

With this information, we can see why Axiata Group Berhad is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Axiata Group Berhad's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Plus, you should also learn about these 2 warning signs we've spotted with Axiata Group Berhad (including 1 which is concerning).

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:AXIATA

Axiata Group Berhad

An investment holding company, provides telecommunications services.

Slightly overvalued with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor