Advertisement

- Malaysia

- /

- Electronic Equipment and Components

- /

- KLSE:SKPRES

Take Care Before Jumping Onto SKP Resources Bhd (KLSE:SKPRES) Even Though It's 31% Cheaper

Unfortunately for some shareholders, the SKP Resources Bhd (KLSE:SKPRES) share price has dived 31% in the last thirty days, prolonging recent pain. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 24% share price drop.

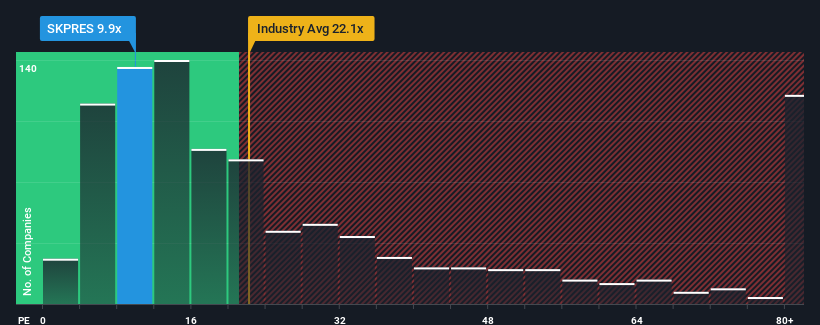

In spite of the heavy fall in price, SKP Resources Bhd may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 9.9x, since almost half of all companies in Malaysia have P/E ratios greater than 15x and even P/E's higher than 24x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

SKP Resources Bhd certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for SKP Resources Bhd

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like SKP Resources Bhd's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 22% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 31% drop in EPS in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the seven analysts covering the company suggest earnings should grow by 23% per year over the next three years. That's shaping up to be materially higher than the 9.6% per year growth forecast for the broader market.

With this information, we find it odd that SKP Resources Bhd is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Bottom Line On SKP Resources Bhd's P/E

The softening of SKP Resources Bhd's shares means its P/E is now sitting at a pretty low level. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that SKP Resources Bhd currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

It is also worth noting that we have found 1 warning sign for SKP Resources Bhd that you need to take into consideration.

If these risks are making you reconsider your opinion on SKP Resources Bhd, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SKPRES

SKP Resources Bhd

Provides electronics manufacturing services (EMS) in Malaysia.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor