Stock Analysis

- Malaysia

- /

- Electronic Equipment and Components

- /

- KLSE:ATAIMS

Despite shrinking by RM90m in the past week, ATA IMS Berhad (KLSE:ATAIMS) shareholders are still up 85% over 1 year

It's been a soft week for ATA IMS Berhad (KLSE:ATAIMS) shares, which are down 14%. But that doesn't change the reality that over twelve months the stock has done really well. To wit, it had solidly beat the market, up 85%.

While the stock has fallen 14% this week, it's worth focusing on the longer term and seeing if the stocks historical returns have been driven by the underlying fundamentals.

Check out our latest analysis for ATA IMS Berhad

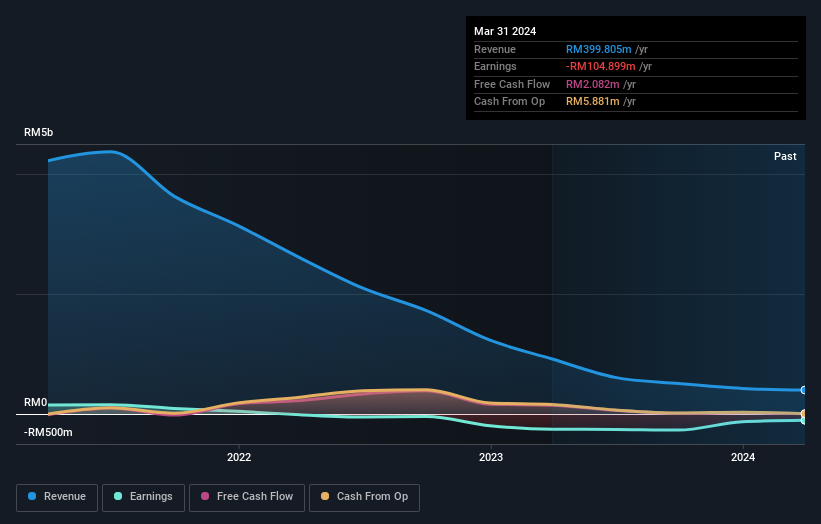

Given that ATA IMS Berhad didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually desire strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

ATA IMS Berhad actually shrunk its revenue over the last year, with a reduction of 56%. Despite the lack of revenue growth, the stock has returned a solid 85% the last twelve months. We can correlate the share price rise with revenue or profit growth, but it seems the market had previously expected weaker results, and sentiment around the stock is improving.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Take a more thorough look at ATA IMS Berhad's financial health with this free report on its balance sheet.

A Different Perspective

We're pleased to report that ATA IMS Berhad shareholders have received a total shareholder return of 85% over one year. That certainly beats the loss of about 11% per year over the last half decade. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. It's always interesting to track share price performance over the longer term. But to understand ATA IMS Berhad better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with ATA IMS Berhad , and understanding them should be part of your investment process.

But note: ATA IMS Berhad may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Malaysian exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether ATA IMS Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether ATA IMS Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:ATAIMS

ATA IMS Berhad

An investment holding company, provides electronics manufacturing services in Malaysia.

Adequate balance sheet and slightly overvalued.