Advertisement

- Malaysia

- /

- Semiconductors

- /

- KLSE:GREATEC

Greatech Technology Berhad (KLSE:GREATEC) Has A Rock Solid Balance Sheet

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Greatech Technology Berhad (KLSE:GREATEC) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Greatech Technology Berhad

What Is Greatech Technology Berhad's Net Debt?

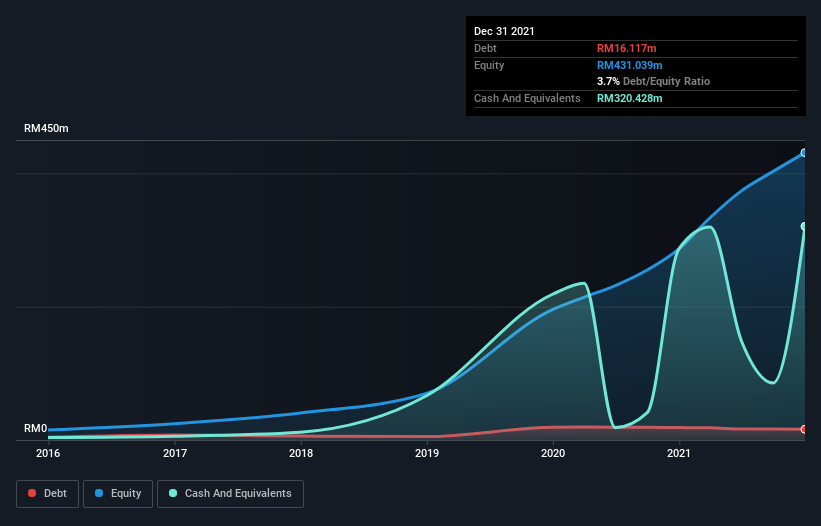

The image below, which you can click on for greater detail, shows that Greatech Technology Berhad had debt of RM16.1m at the end of December 2021, a reduction from RM18.6m over a year. But it also has RM320.4m in cash to offset that, meaning it has RM304.3m net cash.

How Strong Is Greatech Technology Berhad's Balance Sheet?

The latest balance sheet data shows that Greatech Technology Berhad had liabilities of RM150.3m due within a year, and liabilities of RM27.3m falling due after that. Offsetting these obligations, it had cash of RM320.4m as well as receivables valued at RM96.6m due within 12 months. So it can boast RM239.4m more liquid assets than total liabilities.

This surplus suggests that Greatech Technology Berhad has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Greatech Technology Berhad boasts net cash, so it's fair to say it does not have a heavy debt load!

In addition to that, we're happy to report that Greatech Technology Berhad has boosted its EBIT by 58%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Greatech Technology Berhad's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Greatech Technology Berhad has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Greatech Technology Berhad generated free cash flow amounting to a very robust 97% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Summing up

While it is always sensible to investigate a company's debt, in this case Greatech Technology Berhad has RM304.3m in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of RM81m, being 97% of its EBIT. So we don't think Greatech Technology Berhad's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with Greatech Technology Berhad (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:GREATEC

Greatech Technology Berhad

An investment holding company, engages in the design and construction of customized factory automation solutions and system integration.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

39 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

59 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AE

Aequitas on ASML Holding ·

ASML Will Reign as the Kingpin of the Semiconductor Supply Chain

Fair Value:€1.87k16.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AE

Aequitas on Fortinet ·

Fortinet, compounding Cyber Security Player.

Fair Value:US$116.8430.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AE

Aequitas on Constellation Software ·

Constellation Software: A Proven Serial Acquirer at a Discount

Fair Value:CA$3.72k28.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

74 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23039.0% overvalued

94 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OL

oliver_7vepl on Canadian Natural Resources ·

The omission of the effect of the Iran conflict is noteworthy as Canadian Natural Resources is benefiting from it due to its non-participation in the Strait of Hormuz blockade but its use of the pipeline via Vancouver with its delivery of crude to Singapore, Malaysia, Japan,, China, etc. and pricing its delivery in the Brent price relative to WTI and add to it the uptrend of the price of crude.

0

|0