Advertisement

- Malaysia

- /

- Semiconductors

- /

- KLSE:D&O

We Think D & O Green Technologies Berhad (KLSE:D&O) Can Stay On Top Of Its Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that D & O Green Technologies Berhad (KLSE:D&O) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for D & O Green Technologies Berhad

How Much Debt Does D & O Green Technologies Berhad Carry?

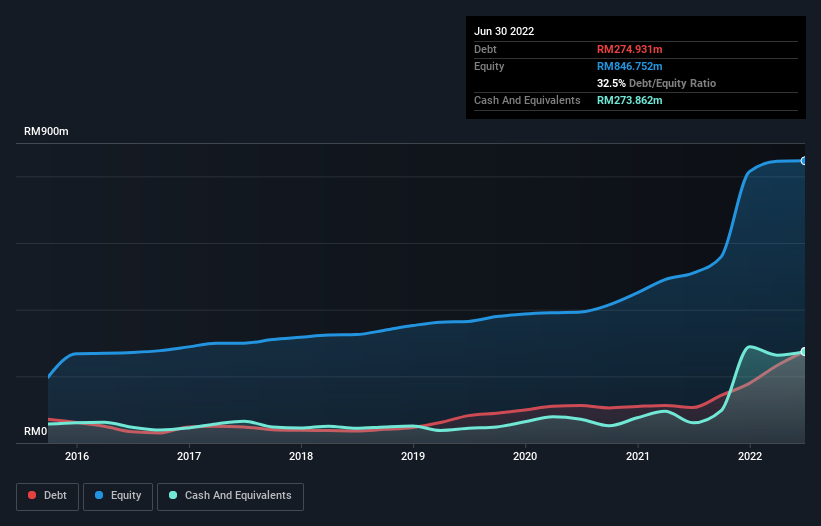

As you can see below, at the end of June 2022, D & O Green Technologies Berhad had RM274.9m of debt, up from RM106.4m a year ago. Click the image for more detail. However, because it has a cash reserve of RM273.9m, its net debt is less, at about RM1.07m.

A Look At D & O Green Technologies Berhad's Liabilities

Zooming in on the latest balance sheet data, we can see that D & O Green Technologies Berhad had liabilities of RM482.4m due within 12 months and liabilities of RM121.7m due beyond that. Offsetting this, it had RM273.9m in cash and RM268.6m in receivables that were due within 12 months. So it has liabilities totalling RM61.6m more than its cash and near-term receivables, combined.

This state of affairs indicates that D & O Green Technologies Berhad's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the RM6.31b company is struggling for cash, we still think it's worth monitoring its balance sheet. But either way, D & O Green Technologies Berhad has virtually no net debt, so it's fair to say it does not have a heavy debt load!

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

D & O Green Technologies Berhad has barely any net debt, as demonstrated by its net debt to EBITDA ratio of only 0.0044. Humorously, it actually received more in interest over the last twelve months than it had to pay. So there's no doubt this company can take on debt as easily as enthusiastic spray-tanners take on an orange hue. Also good is that D & O Green Technologies Berhad grew its EBIT at 11% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if D & O Green Technologies Berhad can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, D & O Green Technologies Berhad burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Happily, D & O Green Technologies Berhad's impressive interest cover implies it has the upper hand on its debt. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. All these things considered, it appears that D & O Green Technologies Berhad can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for D & O Green Technologies Berhad (1 shouldn't be ignored) you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:D&O

D & O Green Technologies Berhad

Through its subsidiary Dominant Opto Technologies Sdn Bhd, manufactures and sells automotive surface mount technology light emitting diodes in Asia, Europe, North Americas, and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor