Advertisement

- Malaysia

- /

- Semiconductors

- /

- KLSE:D&O

Risks To Shareholder Returns Are Elevated At These Prices For D & O Green Technologies Berhad (KLSE:D&O)

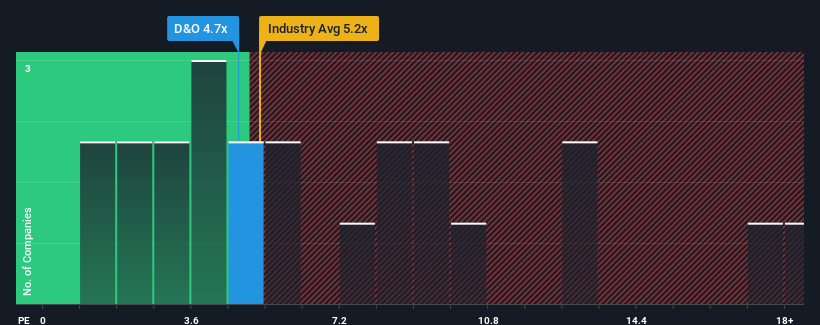

With a median price-to-sales (or "P/S") ratio of close to 5.2x in the Semiconductor industry in Malaysia, you could be forgiven for feeling indifferent about D & O Green Technologies Berhad's (KLSE:D&O) P/S ratio of 4.7x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for D & O Green Technologies Berhad

How D & O Green Technologies Berhad Has Been Performing

With its revenue growth in positive territory compared to the declining revenue of most other companies, D & O Green Technologies Berhad has been doing quite well of late. Perhaps the market is expecting its current strong performance to taper off in accordance to the rest of the industry, which has kept the P/S contained. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on D & O Green Technologies Berhad.What Are Revenue Growth Metrics Telling Us About The P/S?

In order to justify its P/S ratio, D & O Green Technologies Berhad would need to produce growth that's similar to the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 3.4%. The latest three year period has also seen an excellent 77% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 14% per annum during the coming three years according to the six analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 20% each year, which is noticeably more attractive.

With this in mind, we find it intriguing that D & O Green Technologies Berhad's P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Final Word

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Given that D & O Green Technologies Berhad's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for D & O Green Technologies Berhad that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:D&O

D & O Green Technologies Berhad

Through its subsidiary Dominant Opto Technologies Sdn Bhd, manufactures and sells automotive surface mount technology light emitting diodes in Asia, Europe, North Americas, and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor