Stock Analysis

- Malaysia

- /

- Real Estate

- /

- KLSE:THRIVEN

Should You Use Thriven Global Berhad's (KLSE:THRIVEN) Statutory Earnings To Analyse It?

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. In this article, we'll look at how useful this year's statutory profit is, when analysing Thriven Global Berhad (KLSE:THRIVEN).

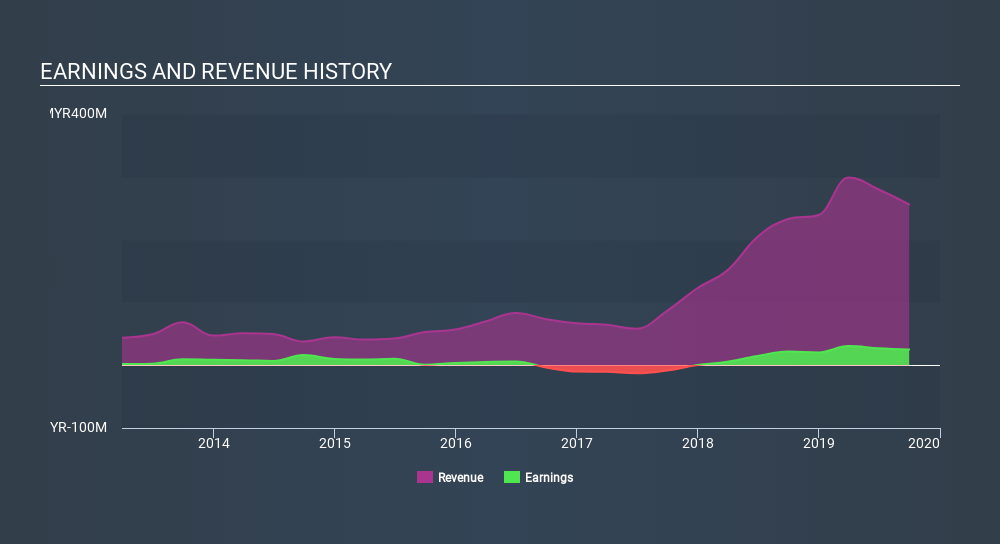

It's good to see that over the last twelve months Thriven Global Berhad made a profit of RM25.1m on revenue of RM255.9m. The chart below shows that revenue has improved over the last three years, and, even better, the company has moved from unprofitable to profitable.

Check out our latest analysis for Thriven Global Berhad

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. In this article we will consider how Thriven Global Berhad's decision to issue new shares in the company has impacted returns to shareholders. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Thriven Global Berhad.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, Thriven Global Berhad issued 5.9% more new shares over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Thriven Global Berhad's EPS by clicking here.

How Is Dilution Impacting Thriven Global Berhad's Earnings Per Share? (EPS)

Thriven Global Berhad was losing money three years ago. On the bright side, in the last twelve months it grew profit by 16%. On the other hand, earnings per share are only up 9.5% over the same period. So you can see that the dilution has had a bit of an impact on shareholders.Therefore, the dilution is having a noteworthy influence on shareholder returnsAnd so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So it will certainly be a positive for shareholders if Thriven Global Berhad can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Thriven Global Berhad's Profit Performance

Each Thriven Global Berhad share now gets a meaningfully smaller slice of its overall profit, due to dilution of existing shareholders. Therefore, it seems possible to us that Thriven Global Berhad's true underlying earnings power is actually less than its statutory profit. But at least holders can take some solace from the 9.5% EPS growth in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. While earnings are important, another area to consider is the balance sheet. If you want to,you can see our take on Thriven Global Berhad's balance sheet by clicking here.

This note has only looked at a single factor that sheds light on the nature of Thriven Global Berhad's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KLSE:THRIVEN

Thriven Global Berhad

An investment holding company, develops and invests in properties in Malaysia.

Adequate balance sheet and slightly overvalued.