Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Tanco Holdings Berhad (KLSE:TANCO) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Tanco Holdings Berhad

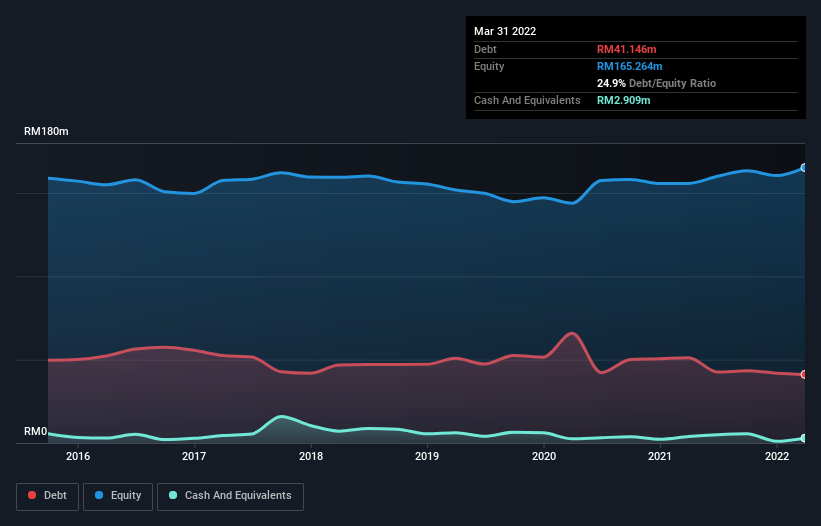

How Much Debt Does Tanco Holdings Berhad Carry?

The image below, which you can click on for greater detail, shows that Tanco Holdings Berhad had debt of RM41.1m at the end of March 2022, a reduction from RM51.2m over a year. On the flip side, it has RM2.91m in cash leading to net debt of about RM38.2m.

How Healthy Is Tanco Holdings Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Tanco Holdings Berhad had liabilities of RM80.3m due within 12 months and liabilities of RM32.0m due beyond that. On the other hand, it had cash of RM2.91m and RM7.30m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM102.1m.

Tanco Holdings Berhad has a market capitalization of RM454.3m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Tanco Holdings Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Tanco Holdings Berhad wasn't profitable at an EBIT level, but managed to grow its revenue by 149%, to RM7.1m. So its pretty obvious shareholders are hoping for more growth!

Caveat Emptor

While we can certainly appreciate Tanco Holdings Berhad's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Indeed, it lost RM13m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through RM17m of cash over the last year. So suffice it to say we do consider the stock to be risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Tanco Holdings Berhad is showing 5 warning signs in our investment analysis , and 3 of those are a bit unpleasant...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Tanco Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TANCO

Tanco Holdings Berhad

An investment holding company, engages in the property development business primarily in Malaysia.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor