Advertisement

- Malaysia

- /

- Real Estate

- /

- KLSE:ECOFIRS

Shareholders Will Most Likely Find EcoFirst Consolidated Bhd's (KLSE:ECOFIRS) CEO Compensation Acceptable

Despite EcoFirst Consolidated Bhd's (KLSE:ECOFIRS) share price growing positively in the past few years, the per-share earnings growth has not grown to investors' expectations, suggesting that there could be other factors at play driving the share price. Some of these issues will occupy shareholders' minds as the AGM rolls around on 27 October 2021. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. In our analysis below, we show why shareholders may consider holding off a raise for the CEO's compensation until company performance improves.

View our latest analysis for EcoFirst Consolidated Bhd

How Does Total Compensation For Kwing Tiong Compare With Other Companies In The Industry?

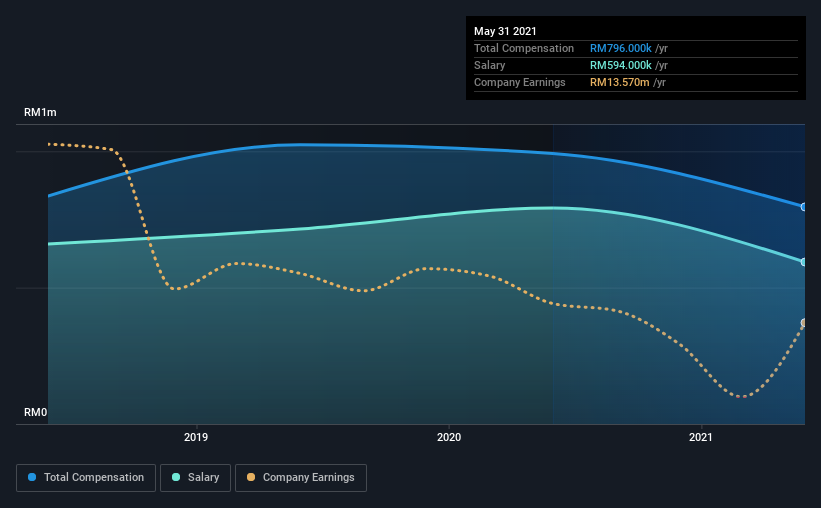

According to our data, EcoFirst Consolidated Bhd has a market capitalization of RM436m, and paid its CEO total annual compensation worth RM796k over the year to May 2021. Notably, that's a decrease of 20% over the year before. Notably, the salary which is RM594.0k, represents most of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations under RM831m, the reported median total CEO compensation was RM703k. From this we gather that Kwing Tiong is paid around the median for CEOs in the industry. Moreover, Kwing Tiong also holds RM50m worth of EcoFirst Consolidated Bhd stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | RM594k | RM792k | 75% |

| Other | RM202k | RM200k | 25% |

| Total Compensation | RM796k | RM992k | 100% |

Talking in terms of the industry, salary represented approximately 76% of total compensation out of all the companies we analyzed, while other remuneration made up 24% of the pie. Our data reveals that EcoFirst Consolidated Bhd allocates salary more or less in line with the wider market. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at EcoFirst Consolidated Bhd's Growth Numbers

Over the last three years, EcoFirst Consolidated Bhd has shrunk its earnings per share by 40% per year. Its revenue is down 72% over the previous year.

The decline in EPS is a bit concerning. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has EcoFirst Consolidated Bhd Been A Good Investment?

EcoFirst Consolidated Bhd has generated a total shareholder return of 32% over three years, so most shareholders would be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

While it's true that shareholders have owned decent returns, it's hard to overlook the lack of earnings growth and this makes us question whether these returns will continue. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We did our research and identified 3 warning signs (and 2 which are a bit concerning) in EcoFirst Consolidated Bhd we think you should know about.

Important note: EcoFirst Consolidated Bhd is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if EcoFirst Consolidated Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:ECOFIRS

EcoFirst Consolidated Bhd

An investment holding company, engages in property construction, development, investment, and management businesses in Malaysia.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor