Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Tropicana Corporation Berhad (KLSE:TROP) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tropicana Corporation Berhad

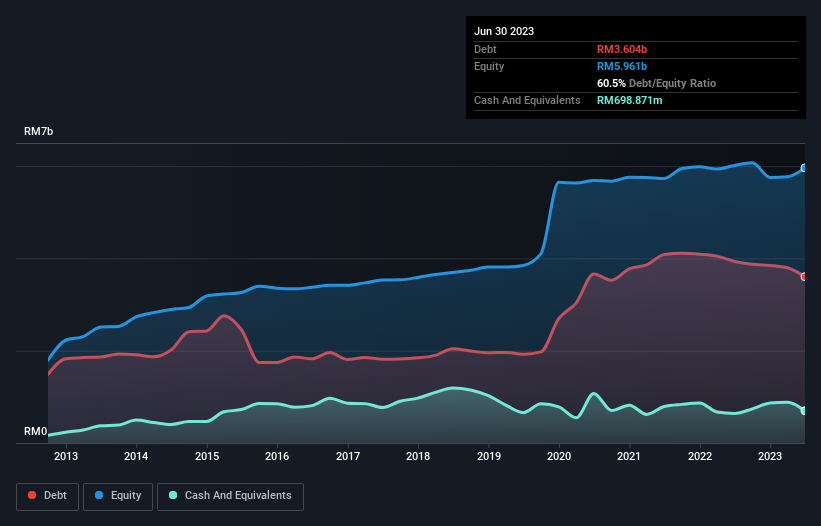

How Much Debt Does Tropicana Corporation Berhad Carry?

You can click the graphic below for the historical numbers, but it shows that Tropicana Corporation Berhad had RM3.60b of debt in June 2023, down from RM3.93b, one year before. On the flip side, it has RM698.9m in cash leading to net debt of about RM2.91b.

How Strong Is Tropicana Corporation Berhad's Balance Sheet?

We can see from the most recent balance sheet that Tropicana Corporation Berhad had liabilities of RM2.93b falling due within a year, and liabilities of RM3.56b due beyond that. On the other hand, it had cash of RM698.9m and RM927.7m worth of receivables due within a year. So its liabilities total RM4.86b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the RM2.81b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Tropicana Corporation Berhad would likely require a major re-capitalisation if it had to pay its creditors today. There's no doubt that we learn most about debt from the balance sheet. But it is Tropicana Corporation Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Tropicana Corporation Berhad reported revenue of RM1.2b, which is a gain of 40%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Despite the top line growth, Tropicana Corporation Berhad still had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at RM195m. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. It's fair to say the loss of RM346m didn't encourage us either; we'd like to see a profit. And until that time we think this is a risky stock. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Tropicana Corporation Berhad (2 are significant!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Tropicana Corporation Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TROP

Tropicana Corporation Berhad

Engages in the property development businesses in Malaysia.

Adequate balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor