Advertisement

- Malaysia

- /

- Real Estate

- /

- KLSE:SIMEPROP

Sime Darby Property Berhad (KLSE:SIMEPROP) Is Due To Pay A Dividend Of MYR0.01

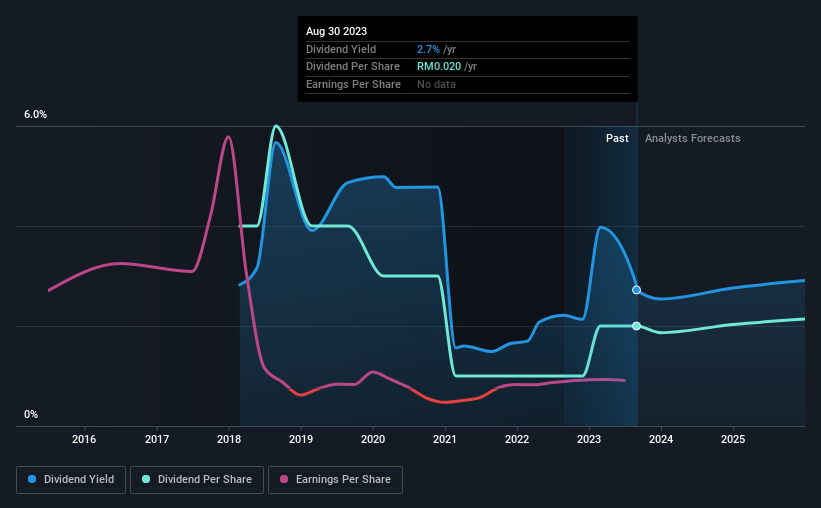

The board of Sime Darby Property Berhad (KLSE:SIMEPROP) has announced that it will pay a dividend on the 19th of October, with investors receiving MYR0.01 per share. Including this payment, the dividend yield on the stock will be 2.7%, which is a modest boost for shareholders' returns.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Sime Darby Property Berhad's stock price has increased by 60% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Sime Darby Property Berhad

Sime Darby Property Berhad's Dividend Is Well Covered By Earnings

Even a low dividend yield can be attractive if it is sustained for years on end. Prior to this announcement, Sime Darby Property Berhad's dividend was comfortably covered by both cash flow and earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Looking forward, earnings per share is forecast to rise by 27.7% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could be 20% by next year, which is in a pretty sustainable range.

Sime Darby Property Berhad's Dividend Has Lacked Consistency

Sime Darby Property Berhad has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The annual payment during the last 5 years was MYR0.04 in 2018, and the most recent fiscal year payment was MYR0.02. Dividend payments have fallen sharply, down 50% over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS is growing. Over the past five years, it looks as though Sime Darby Property Berhad's EPS has declined at around 17% a year. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

Our Thoughts On Sime Darby Property Berhad's Dividend

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We don't think Sime Darby Property Berhad is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for Sime Darby Property Berhad that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SIMEPROP

Sime Darby Property Berhad

An investment holding company, engages in the property development business in Malaysia, Singapore, and the United Kingdom.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor