Advertisement

- Malaysia

- /

- Metals and Mining

- /

- KLSE:MSC

Not Many Are Piling Into Malaysia Smelting Corporation Berhad (KLSE:MSC) Stock Yet As It Plummets 27%

Malaysia Smelting Corporation Berhad (KLSE:MSC) shareholders that were waiting for something to happen have been dealt a blow with a 27% share price drop in the last month. Longer-term shareholders would now have taken a real hit with the stock declining 5.8% in the last year.

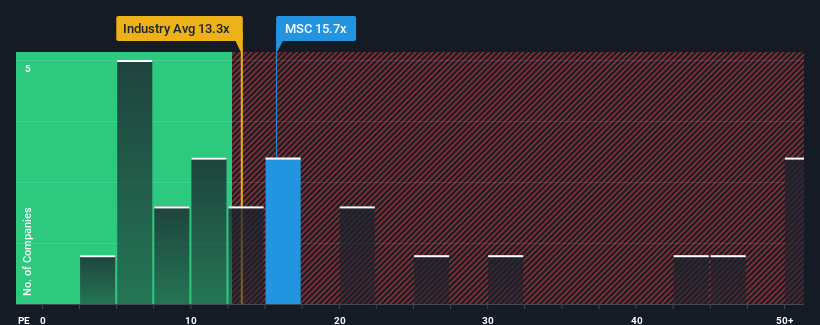

In spite of the heavy fall in price, you could still be forgiven for feeling indifferent about Malaysia Smelting Corporation Berhad's P/E ratio of 15.7x, since the median price-to-earnings (or "P/E") ratio in Malaysia is also close to 17x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Malaysia Smelting Corporation Berhad could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

See our latest analysis for Malaysia Smelting Corporation Berhad

Is There Some Growth For Malaysia Smelting Corporation Berhad?

In order to justify its P/E ratio, Malaysia Smelting Corporation Berhad would need to produce growth that's similar to the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 3.8%. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 38% per year during the coming three years according to the one analyst following the company. With the market only predicted to deliver 14% per annum, the company is positioned for a stronger earnings result.

In light of this, it's curious that Malaysia Smelting Corporation Berhad's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Malaysia Smelting Corporation Berhad's P/E

With its share price falling into a hole, the P/E for Malaysia Smelting Corporation Berhad looks quite average now. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Malaysia Smelting Corporation Berhad currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Before you take the next step, you should know about the 1 warning sign for Malaysia Smelting Corporation Berhad that we have uncovered.

Of course, you might also be able to find a better stock than Malaysia Smelting Corporation Berhad. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:MSC

Malaysia Smelting Corporation Berhad

An investment holding company, engages in the smelting tin concentrates and tin bearing materials primarily in Malaysia.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor