Advertisement

- Malaysia

- /

- Metals and Mining

- /

- KLSE:KSSC

We Believe K. Seng Seng Corporation Berhad's (KLSE:KSSC) Earnings Are A Poor Guide For Its Profitability

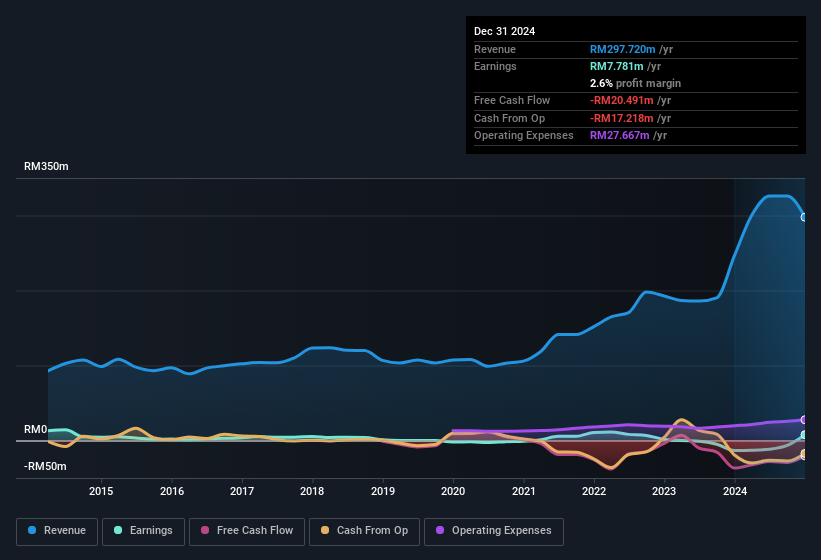

Despite posting strong earnings, K. Seng Seng Corporation Berhad's (KLSE:KSSC) stock didn't move much over the last week. We looked deeper into the numbers and found that shareholders might be concerned with some underlying weaknesses.

View our latest analysis for K. Seng Seng Corporation Berhad

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, K. Seng Seng Corporation Berhad increased the number of shares on issue by 23% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out K. Seng Seng Corporation Berhad's historical EPS growth by clicking on this link.

How Is Dilution Impacting K. Seng Seng Corporation Berhad's Earnings Per Share (EPS)?

We don't have any data on the company's profits from three years ago. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. What we do know is that while it's great to see a profit over the last twelve months, that profit would have been better, on a per share basis, if the company hadn't needed to issue shares. And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, if K. Seng Seng Corporation Berhad's earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of K. Seng Seng Corporation Berhad.

How Do Unusual Items Influence Profit?

Alongside that dilution, it's also important to note that K. Seng Seng Corporation Berhad's profit was boosted by unusual items worth RM9.6m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. K. Seng Seng Corporation Berhad had a rather significant contribution from unusual items relative to its profit to December 2024. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On K. Seng Seng Corporation Berhad's Profit Performance

In its last report K. Seng Seng Corporation Berhad benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. Considering all this we'd argue K. Seng Seng Corporation Berhad's profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about K. Seng Seng Corporation Berhad as a business, it's important to be aware of any risks it's facing. Case in point: We've spotted 4 warning signs for K. Seng Seng Corporation Berhad you should be mindful of and 1 of these is potentially serious.

Our examination of K. Seng Seng Corporation Berhad has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if K. Seng Seng Corporation Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KSSC

K. Seng Seng Corporation Berhad

An investment holding company, engages in the manufacture and processing of secondary stainless steel and other metal related products in Malaysia, the Republic of Singapore, Australia, the Republic of Indonesia, and Brunei.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor