Advertisement

- Malaysia

- /

- Household Products

- /

- KLSE:HEXCARE

Rubberex Corporation (M) Berhad's (KLSE:RUBEREX) Stock Has Been Sliding But Fundamentals Look Strong: Is The Market Wrong?

With its stock down 39% over the past three months, it is easy to disregard Rubberex Corporation (M) Berhad (KLSE:RUBEREX). However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. Particularly, we will be paying attention to Rubberex Corporation (M) Berhad's ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Rubberex Corporation (M) Berhad

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Rubberex Corporation (M) Berhad is:

35% = RM131m ÷ RM378m (Based on the trailing twelve months to December 2020).

The 'return' refers to a company's earnings over the last year. So, this means that for every MYR1 of its shareholder's investments, the company generates a profit of MYR0.35.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

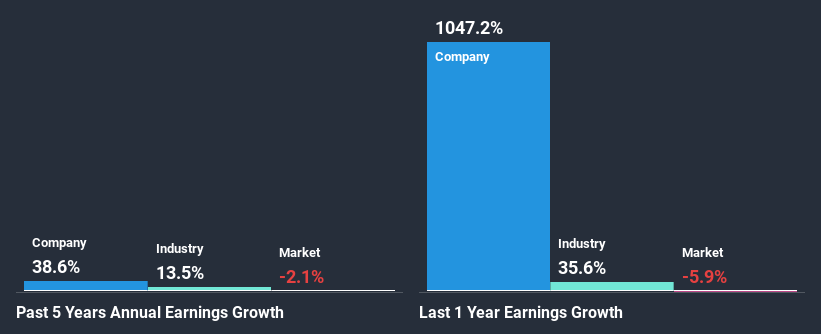

Rubberex Corporation (M) Berhad's Earnings Growth And 35% ROE

Firstly, we acknowledge that Rubberex Corporation (M) Berhad has a significantly high ROE. Secondly, even when compared to the industry average of 14% the company's ROE is quite impressive. Under the circumstances, Rubberex Corporation (M) Berhad's considerable five year net income growth of 39% was to be expected.

Next, on comparing with the industry net income growth, we found that Rubberex Corporation (M) Berhad's growth is quite high when compared to the industry average growth of 7.1% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Rubberex Corporation (M) Berhad's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Rubberex Corporation (M) Berhad Using Its Retained Earnings Effectively?

While the company did pay out a portion of its dividend in the past, it currently doesn't pay a dividend. This is likely what's driving the high earnings growth number discussed above.

Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 69% over the next three years. Consequently, the higher expected payout ratio explains the decline in the company's expected ROE (to 13%) over the same period.

Conclusion

Overall, we are quite pleased with Rubberex Corporation (M) Berhad's performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. Having said that, on studying current analyst estimates, we were concerned to see that while the company has grown its earnings in the past, analysts expect its earnings to shrink in the future. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

When trading Rubberex Corporation (M) Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hextar Healthcare Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:HEXCARE

Hextar Healthcare Berhad

An investment holding company, produces, sells, and exports household gloves, industrial gloves, and nitrile disposable gloves in Europe, Asia, North and South America, and internationally.

Adequate balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor