Advertisement

- Malaysia

- /

- Healthcare Services

- /

- KLSE:HONGSENG

Health Check: How Prudently Does Hong Seng Consolidated Berhad (KLSE:HONGSENG) Use Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Hong Seng Consolidated Berhad (KLSE:HONGSENG) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Hong Seng Consolidated Berhad

What Is Hong Seng Consolidated Berhad's Debt?

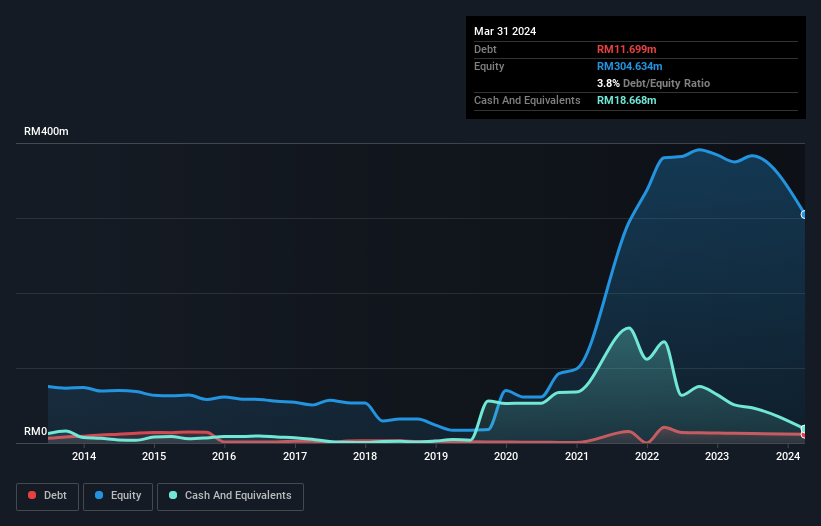

The image below, which you can click on for greater detail, shows that Hong Seng Consolidated Berhad had debt of RM11.7m at the end of March 2024, a reduction from RM13.0m over a year. However, it does have RM18.7m in cash offsetting this, leading to net cash of RM6.97m.

A Look At Hong Seng Consolidated Berhad's Liabilities

We can see from the most recent balance sheet that Hong Seng Consolidated Berhad had liabilities of RM20.2m falling due within a year, and liabilities of RM22.8m due beyond that. On the other hand, it had cash of RM18.7m and RM103.1m worth of receivables due within a year. So it can boast RM78.7m more liquid assets than total liabilities.

This excess liquidity is a great indication that Hong Seng Consolidated Berhad's balance sheet is almost as strong as Fort Knox. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Succinctly put, Hong Seng Consolidated Berhad boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is Hong Seng Consolidated Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Hong Seng Consolidated Berhad reported revenue of RM15m, which is a gain of 29%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Hong Seng Consolidated Berhad?

Although Hong Seng Consolidated Berhad had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of RM4.8m. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. Given it also grew revenue by 29% over the last year, we think there's a good chance the company is on track. So this may well be an interesting business to watch grow. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Hong Seng Consolidated Berhad (including 1 which is potentially serious) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Hong Seng Consolidated Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HONGSENG

Hong Seng Consolidated Berhad

An investment holding company, engages in gloves and NBL manufacturing, healthcare, and financial services in Malaysia and Australia.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor