Advertisement

Nestlé (Malaysia) Berhad's (KLSE:NESTLE) Business Is Yet to Catch Up With Its Share Price

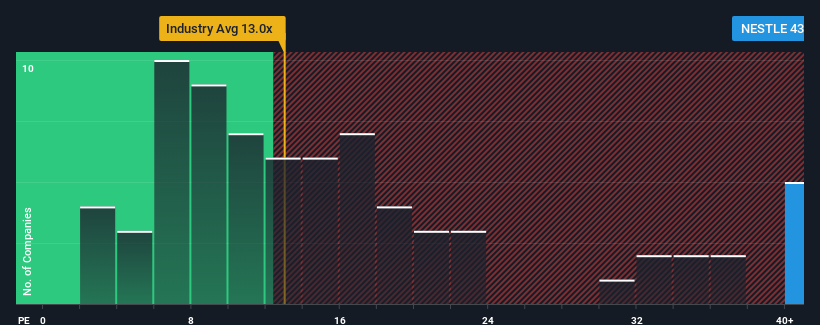

When close to half the companies in Malaysia have price-to-earnings ratios (or "P/E's") below 15x, you may consider Nestlé (Malaysia) Berhad (KLSE:NESTLE) as a stock to avoid entirely with its 43.1x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Nestlé (Malaysia) Berhad hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for Nestlé (Malaysia) Berhad

Is There Enough Growth For Nestlé (Malaysia) Berhad?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Nestlé (Malaysia) Berhad's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 8.4%. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 9.7% per year during the coming three years according to the twelve analysts following the company. With the market predicted to deliver 14% growth per year, the company is positioned for a weaker earnings result.

In light of this, it's alarming that Nestlé (Malaysia) Berhad's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From Nestlé (Malaysia) Berhad's P/E?

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Nestlé (Malaysia) Berhad currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Nestlé (Malaysia) Berhad (1 is a bit concerning!) that you need to be mindful of.

If you're unsure about the strength of Nestlé (Malaysia) Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Nestlé (Malaysia) Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:NESTLE

Nestlé (Malaysia) Berhad

Manufactures and sells food and beverage products in Malaysia and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor