Advertisement

Is Keck Seng (Malaysia) Berhad (KLSE:KSENG) Using Debt In A Risky Way?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Keck Seng (Malaysia) Berhad (KLSE:KSENG) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

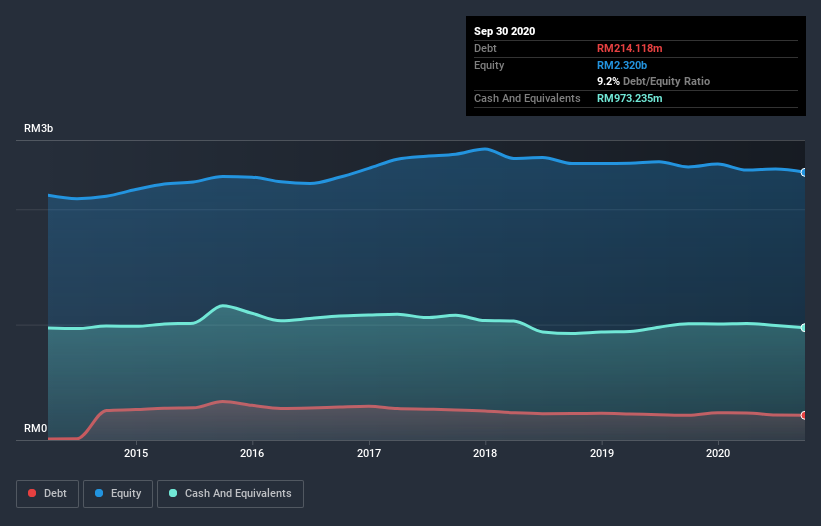

Check out our latest analysis for Keck Seng (Malaysia) Berhad

How Much Debt Does Keck Seng (Malaysia) Berhad Carry?

As you can see below, Keck Seng (Malaysia) Berhad had RM213.9m of debt, at September 2020, which is about the same as the year before. You can click the chart for greater detail. But it also has RM973.2m in cash to offset that, meaning it has RM759.3m net cash.

How Strong Is Keck Seng (Malaysia) Berhad's Balance Sheet?

The latest balance sheet data shows that Keck Seng (Malaysia) Berhad had liabilities of RM171.4m due within a year, and liabilities of RM197.1m falling due after that. On the other hand, it had cash of RM973.2m and RM57.2m worth of receivables due within a year. So it actually has RM662.0m more liquid assets than total liabilities.

This excess liquidity is a great indication that Keck Seng (Malaysia) Berhad's balance sheet is almost as strong as Fort Knox. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Simply put, the fact that Keck Seng (Malaysia) Berhad has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is Keck Seng (Malaysia) Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Keck Seng (Malaysia) Berhad made a loss at the EBIT level, and saw its revenue drop to RM868m, which is a fall of 13%. We would much prefer see growth.

So How Risky Is Keck Seng (Malaysia) Berhad?

Although Keck Seng (Malaysia) Berhad had an earnings before interest and tax (EBIT) loss over the last twelve months, it made a statutory profit of RM2.8m. So taking that on face value, and considering the cash, we don't think its very risky in the near term. There's no doubt the next few years will be crucial to how the business matures. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Keck Seng (Malaysia) Berhad (at least 1 which is a bit concerning) , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Keck Seng (Malaysia) Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Keck Seng (Malaysia) Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:KSENG

Keck Seng (Malaysia) Berhad

Engages in the cultivation and sale of oil palm in Malaysia, Singapore, Hong Kong, Canada, and the United States.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor