Stock Analysis

Here's Why Kuala Lumpur Kepong Berhad (KLSE:KLK) Can Manage Its Debt Responsibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Kuala Lumpur Kepong Berhad (KLSE:KLK) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

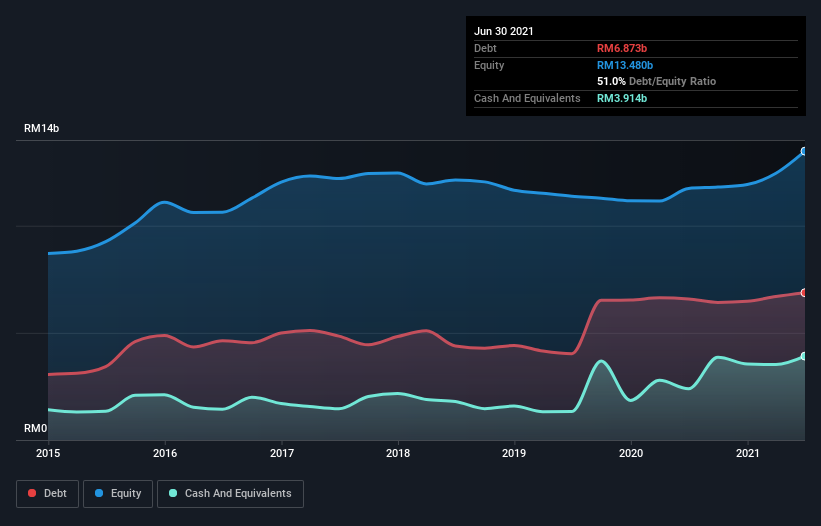

See our latest analysis for Kuala Lumpur Kepong Berhad

What Is Kuala Lumpur Kepong Berhad's Net Debt?

As you can see below, at the end of June 2021, Kuala Lumpur Kepong Berhad had RM6.87b of debt, up from RM6.58b a year ago. Click the image for more detail. However, it also had RM3.91b in cash, and so its net debt is RM2.96b.

How Strong Is Kuala Lumpur Kepong Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kuala Lumpur Kepong Berhad had liabilities of RM3.90b due within 12 months and liabilities of RM6.29b due beyond that. Offsetting these obligations, it had cash of RM3.91b as well as receivables valued at RM2.56b due within 12 months. So its liabilities total RM3.72b more than the combination of its cash and short-term receivables.

Since publicly traded Kuala Lumpur Kepong Berhad shares are worth a total of RM21.7b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 1.1 times EBITDA, Kuala Lumpur Kepong Berhad is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 9.0 times the interest expense over the last year. In addition to that, we're happy to report that Kuala Lumpur Kepong Berhad has boosted its EBIT by 47%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Kuala Lumpur Kepong Berhad's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Kuala Lumpur Kepong Berhad recorded free cash flow of 35% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Happily, Kuala Lumpur Kepong Berhad's impressive EBIT growth rate implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its conversion of EBIT to free cash flow. When we consider the range of factors above, it looks like Kuala Lumpur Kepong Berhad is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Kuala Lumpur Kepong Berhad has 4 warning signs (and 1 which is concerning) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're helping make it simple.

Find out whether Kuala Lumpur Kepong Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:KLK

Kuala Lumpur Kepong Berhad

Engages in the plantation, manufacturing, and property development businesses.

Moderate growth potential with mediocre balance sheet.