Advertisement

Tong Herr Resources Berhad's (KLSE:TONGHER) Dividend Will Be Reduced To MYR0.075

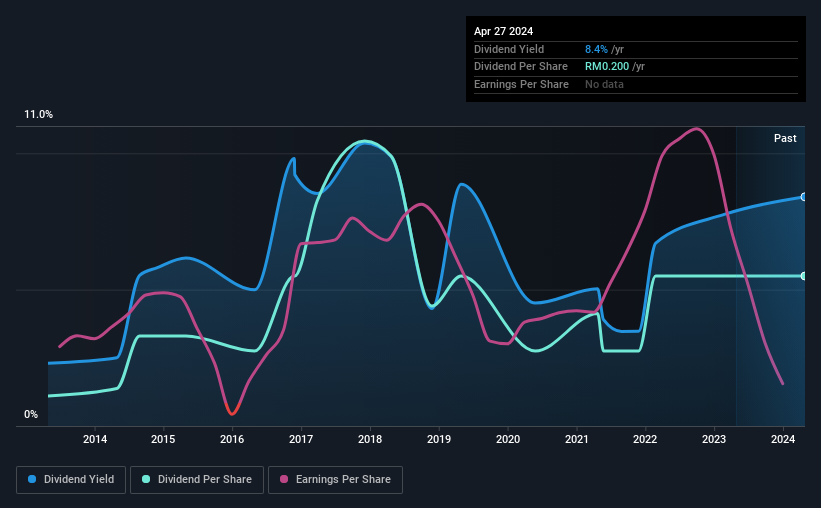

Tong Herr Resources Berhad (KLSE:TONGHER) is reducing its dividend to MYR0.075 on the 14th of Junewhich is 63% less than last year's comparable payment of MYR0.20. However, the dividend yield of 8.4% is still a decent boost to shareholder returns.

Check out our latest analysis for Tong Herr Resources Berhad

Tong Herr Resources Berhad Is Paying Out More Than It Is Earning

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, the company was paying out 157% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 60%. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

If the company can't turn things around, EPS could fall by 36.1% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could reach 294%, which could put the dividend in jeopardy if the company's earnings don't improve.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2014, the annual payment back then was MYR0.04, compared to the most recent full-year payment of MYR0.20. This works out to be a compound annual growth rate (CAGR) of approximately 17% a year over that time. Tong Herr Resources Berhad has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Tong Herr Resources Berhad's EPS has fallen by approximately 36% per year during the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future.

Tong Herr Resources Berhad's Dividend Doesn't Look Sustainable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 3 warning signs for Tong Herr Resources Berhad that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Tong Herr Resources Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TONGHER

Tong Herr Resources Berhad

An investment holding company, manufactures and sells stainless steel fasteners in Malaysia, Thailand, Taiwan, the United States, and internationally.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor