Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:PRTASCO

Is There More Growth In Store For Protasco Berhad's (KLSE:PRTASCO) Returns On Capital?

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So when we looked at Protasco Berhad (KLSE:PRTASCO) and its trend of ROCE, we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Protasco Berhad is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

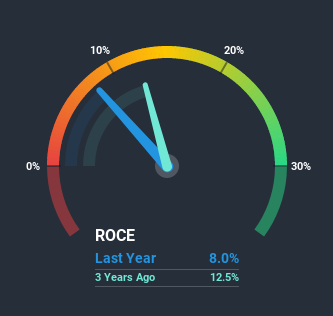

0.08 = RM37m ÷ (RM1.2b - RM775m) (Based on the trailing twelve months to September 2020).

So, Protasco Berhad has an ROCE of 8.0%. In absolute terms, that's a low return, but it's much better than the Construction industry average of 5.2%.

See our latest analysis for Protasco Berhad

In the above chart we have measured Protasco Berhad's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Protasco Berhad's ROCE Trending?

You'd find it hard not to be impressed with the ROCE trend at Protasco Berhad. The data shows that returns on capital have increased by 60% over the trailing five years. That's not bad because this tells for every dollar invested (capital employed), the company is increasing the amount earned from that dollar. In regards to capital employed, Protasco Berhad appears to been achieving more with less, since the business is using 27% less capital to run its operation. If this trend continues, the business might be getting more efficient but it's shrinking in terms of total assets.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. The current liabilities has increased to 63% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. And with current liabilities at those levels, that's pretty high.Our Take On Protasco Berhad's ROCE

In summary, it's great to see that Protasco Berhad has been able to turn things around and earn higher returns on lower amounts of capital. However the stock is down a substantial 71% in the last five years so there could be other areas of the business hurting its prospects. Still, it's worth doing some further research to see if the trends will continue into the future.

One more thing: We've identified 3 warning signs with Protasco Berhad (at least 1 which is significant) , and understanding them would certainly be useful.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you decide to trade Protasco Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:PRTASCO

Protasco Berhad

An investment holding company, provides infrastructure solutions in Malaysia.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor