Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:NESTCON

Nestcon Berhad (KLSE:NESTCON) Delivered A Weaker ROE Than Its Industry

While some investors are already well versed in financial metrics (hat tip), this article is for those who would like to learn about Return On Equity (ROE) and why it is important. To keep the lesson grounded in practicality, we'll use ROE to better understand Nestcon Berhad (KLSE:NESTCON).

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Nestcon Berhad is:

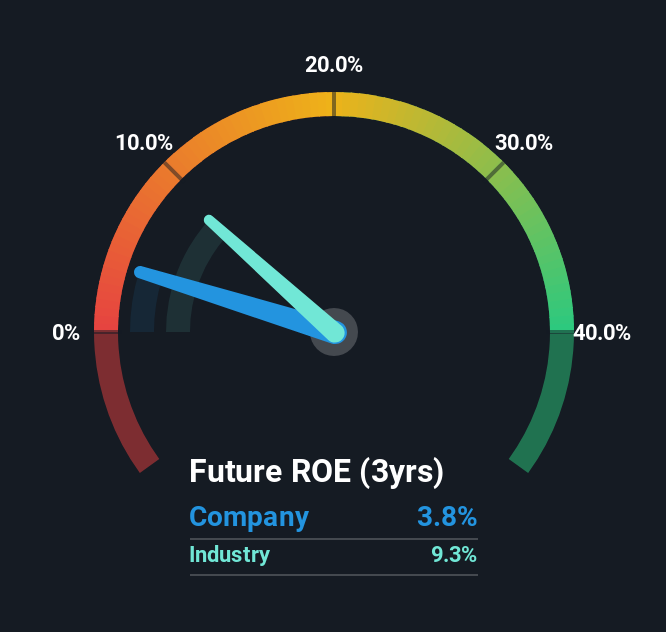

3.8% = RM6.4m ÷ RM168m (Based on the trailing twelve months to September 2025).

The 'return' is the yearly profit. That means that for every MYR1 worth of shareholders' equity, the company generated MYR0.04 in profit.

Check out our latest analysis for Nestcon Berhad

Does Nestcon Berhad Have A Good Return On Equity?

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. As is clear from the image below, Nestcon Berhad has a lower ROE than the average (9.3%) in the Construction industry.

That's not what we like to see. Although, we think that a lower ROE could still mean that a company has the opportunity to better its returns with the use of leverage, provided its existing debt levels are low. A high debt company having a low ROE is a different story altogether and a risky investment in our books. You can see the 3 risks we have identified for Nestcon Berhad by visiting our risks dashboard for free on our platform here.

How Does Debt Impact ROE?

Most companies need money -- from somewhere -- to grow their profits. That cash can come from retained earnings, issuing new shares (equity), or debt. In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders' equity. That will make the ROE look better than if no debt was used.

Combining Nestcon Berhad's Debt And Its 3.8% Return On Equity

It's worth noting the high use of debt by Nestcon Berhad, leading to its debt to equity ratio of 1.04. Its ROE is quite low, even with the use of significant debt; that's not a good result, in our opinion. Debt does bring extra risk, so it's only really worthwhile when a company generates some decent returns from it.

Summary

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. In our books, the highest quality companies have high return on equity, despite low debt. If two companies have the same ROE, then I would generally prefer the one with less debt.

But ROE is just one piece of a bigger puzzle, since high quality businesses often trade on high multiples of earnings. It is important to consider other factors, such as future profit growth -- and how much investment is required going forward. So I think it may be worth checking this free this detailed graph of past earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Nestcon Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:NESTCON

Nestcon Berhad

An investment holding company, provides construction services in Malaysia.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3637.3% undervalued

42 followersusers have followed this narrative

14 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

Marek_Trnka on CSG ·

Czechoslovak Group - is it really so hot?

Fair Value:€5547.3% undervalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

AL

alex30free on Swedencare ·

The Compound Effect: From Acquisition to Integration

Fair Value:SEK 46.2849.1% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$27.0328.7% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on Meta Platforms ·

The Superintelligence Pivot: Meta’s $135 Billion Bet on the Energy-Compute Nexus

Fair Value:US$555.8515.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on Apple ·

The Privacy Fortress: Apple’s Lean AI Path and the $100 Billion Buyback Engine

Fair Value:US$180.6341.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.6% undervalued

59 followersusers have followed this narrative

5 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$603.2233.5% undervalued

1277 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.7% undervalued

1073 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

Trending Discussion

US

User on Tesla ·

When was the last time that Tesla delivered on its promises? Lets go through the list! The last successful would be the Tesla Model 3 which was 2019 with first deliveries 2017. Roadster not shipped. Tesla Cybertruck global roll out failed. They might have a bunch of prototypes (that are being controlled remotely) And you think they'll be able to ship something as complicated as a robot? It's a pure speculation buy.

4

|1

US

User on Tesla ·

This article completely disregards (ignores, forgets) how far China is in this field. If Tesla continues on this path, they will be fighting for their lives trying to sell $40000 dollar robots that can do less than a $10000 dollar one from China will do. Fair value of Tesla? It has always been a hype stock with a valuation completely unbased in reality. Your guess is as good as mine, but especially after the carbon credit scheme got canned, it is downwards of $150.

3

|0

US

User on Tesla ·

There is a lot of Musk's puffery being echoed in this article. "ecosystem dominance", Tesla certainly do not dominate any of their new markets. If Tesla is the undisputed leader of the premium "Closed Garden.", it is only through EV's and that business has been declining year-on-year, despite the market increasing. Vehicle manufactures are finding that customers are rejecting the subscription model. "The Cybercab fleet (launching 2026) acts as the financial bridge.", that is a stretch. Even if Level 4/5 autonomy is achieved, "profitability" still has to be proved, where the competition is not necessarily Waymo, but Uber. Taking the driver out of a ride‑hailing service may not be the killer saving people think it will be. Likewise, outside of CGI and for quite some time, an Optimus humanoid robot may prove more expensive and not as useful, versatile, skilled and knowledgeable as a domestic worker. Telsa may be withdrawing from the EV market, but for its other ventures, they have arrived late to the party, do not lead and show no sign that they will dominate any of them.

2

|0