Advertisement

Hong Leong Financial Group Berhad (KLSE:HLFG) Has Announced That It Will Be Increasing Its Dividend To RM0.15

Hong Leong Financial Group Berhad (KLSE:HLFG) will increase its dividend on the 30th of March to RM0.15, which is 39% higher than last year. Although the dividend is now higher, the yield is only 2.2%, which is below the industry average.

View our latest analysis for Hong Leong Financial Group Berhad

Hong Leong Financial Group Berhad's Dividend Is Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. Prior to this announcement, Hong Leong Financial Group Berhad's earnings easily covered the dividend, but free cash flows were negative. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

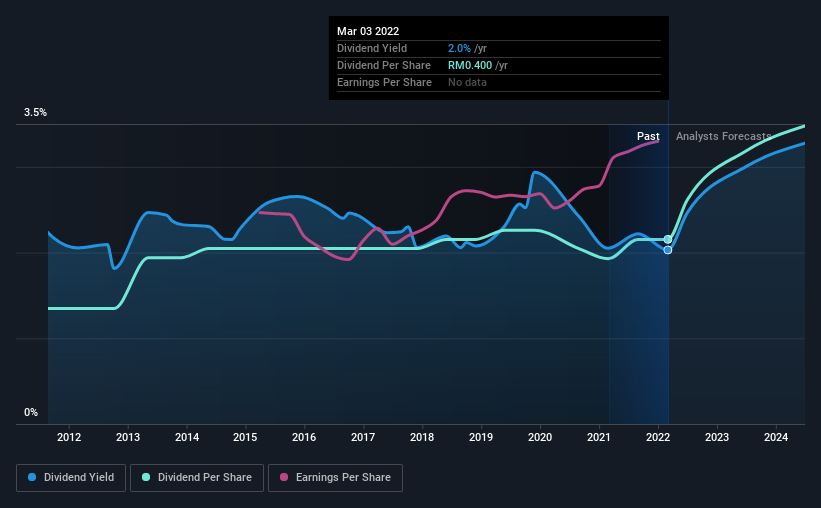

The next year is set to see EPS grow by 4.0%. Assuming the dividend continues along recent trends, we think the payout ratio could be 20% by next year, which is in a pretty sustainable range.

Hong Leong Financial Group Berhad Has A Solid Track Record

The company has an extended history of paying stable dividends. The first annual payment during the last 10 years was RM0.25 in 2012, and the most recent fiscal year payment was RM0.40. This works out to be a compound annual growth rate (CAGR) of approximately 4.8% a year over that time. While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is less attractive.

We Could See Hong Leong Financial Group Berhad's Dividend Growing

The company's investors will be pleased to have been receiving dividend income for some time. It's encouraging to see Hong Leong Financial Group Berhad has been growing its earnings per share at 9.0% a year over the past five years. Hong Leong Financial Group Berhad definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

Our Thoughts On Hong Leong Financial Group Berhad's Dividend

In summary, while it's always good to see the dividend being raised, we don't think Hong Leong Financial Group Berhad's payments are rock solid. While Hong Leong Financial Group Berhad is earning enough to cover the payments, the cash flows are lacking. We would probably look elsewhere for an income investment.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Earnings growth generally bodes well for the future value of company dividend payments. See if the 4 Hong Leong Financial Group Berhad analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hong Leong Financial Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HLFG

Hong Leong Financial Group Berhad

An investment holding company, provides investment banking, stockbroking, and fund management business of financial services to consumer, corporate, and institutional customers.

Very undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor