Advertisement

- Malaysia

- /

- Auto Components

- /

- KLSE:MCEHLDG

We Think You Should Be Aware Of Some Concerning Factors In MCE Holdings Berhad's (KLSE:MCEHLDG) Earnings

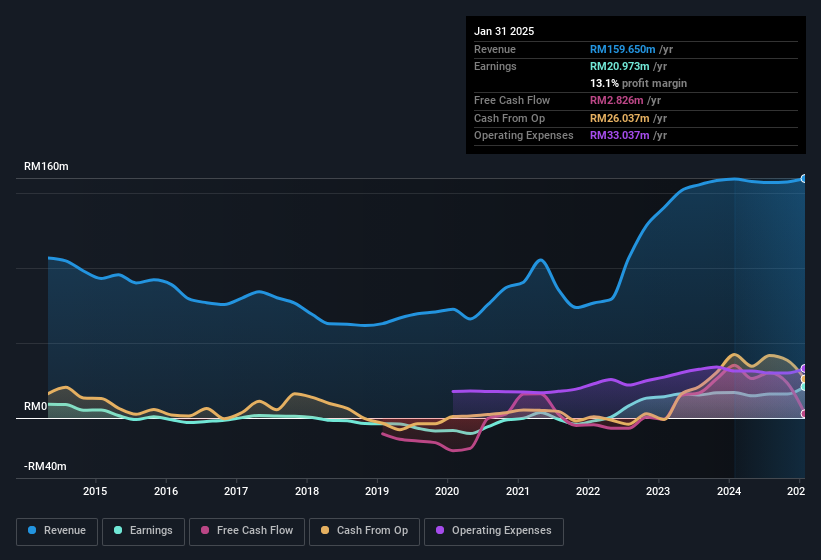

MCE Holdings Berhad's (KLSE:MCEHLDG) healthy profit numbers didn't contain any surprises for investors. However the statutory profit number doesn't tell the whole story, and we have found some factors which might be of concern to shareholders.

Examining Cashflow Against MCE Holdings Berhad's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

MCE Holdings Berhad has an accrual ratio of 0.21 for the year to January 2025. Unfortunately, that means its free cash flow fell significantly short of its reported profits. Indeed, in the last twelve months it reported free cash flow of RM2.8m, which is significantly less than its profit of RM21.0m. MCE Holdings Berhad's free cash flow actually declined over the last year, but it may bounce back next year, since free cash flow is often more volatile than accounting profits. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings. One positive for MCE Holdings Berhad shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of MCE Holdings Berhad.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. As it happens, MCE Holdings Berhad issued 10% more new shares over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of MCE Holdings Berhad's EPS by clicking here.

A Look At The Impact Of MCE Holdings Berhad's Dilution On Its Earnings Per Share (EPS)

MCE Holdings Berhad was losing money three years ago. The good news is that profit was up 23% in the last twelve months. But EPS was less impressive, up only 20% in that time. And so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So MCE Holdings Berhad shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On MCE Holdings Berhad's Profit Performance

As it turns out, MCE Holdings Berhad couldn't match its profit with cashflow and its dilution means that earnings per share growth is lagging net income growth. Considering all this we'd argue MCE Holdings Berhad's profits probably give an overly generous impression of its sustainable level of profitability. So while earnings quality is important, it's equally important to consider the risks facing MCE Holdings Berhad at this point in time. Be aware that MCE Holdings Berhad is showing 3 warning signs in our investment analysis and 1 of those makes us a bit uncomfortable...

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:MCEHLDG

MCE Holdings Berhad

An investment holding company, designs, manufactures, and sells automotive electronics and mechatronics parts in Malaysia.

Flawless balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor