Advertisement

- Luxembourg

- /

- Media

- /

- BDL:SESGL

SES (BDL:SESGL) Has Some Difficulty Using Its Capital Effectively

Ignoring the stock price of a company, what are the underlying trends that tell us a business is past the growth phase? When we see a declining return on capital employed (ROCE) in conjunction with a declining base of capital employed, that's often how a mature business shows signs of aging. This combination can tell you that not only is the company investing less, it's earning less on what it does invest. Having said that, after a brief look, SES (BDL:SESGL) we aren't filled with optimism, but let's investigate further.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for SES, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

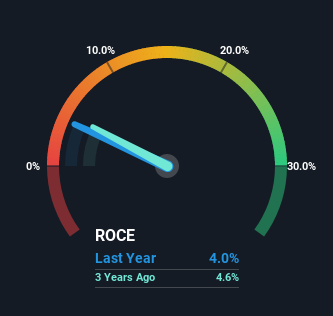

0.04 = €427m ÷ (€13b - €2.5b) (Based on the trailing twelve months to March 2022).

So, SES has an ROCE of 4.0%. In absolute terms, that's a low return and it also under-performs the Media industry average of 11%.

Check out our latest analysis for SES

In the above chart we have measured SES' prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for SES.

What Can We Tell From SES' ROCE Trend?

We are a bit worried about the trend of returns on capital at SES. Unfortunately the returns on capital have diminished from the 6.3% that they were earning five years ago. On top of that, it's worth noting that the amount of capital employed within the business has remained relatively steady. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. If these trends continue, we wouldn't expect SES to turn into a multi-bagger.

The Bottom Line

In summary, it's unfortunate that SES is generating lower returns from the same amount of capital. Long term shareholders who've owned the stock over the last five years have experienced a 50% depreciation in their investment, so it appears the market might not like these trends either. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

One more thing: We've identified 3 warning signs with SES (at least 1 which is a bit concerning) , and understanding them would certainly be useful.

While SES isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BDL:SESGL

SES

Provides satellite-based data transmission capacity and ancillary services worldwide.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1943.7% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7720.5% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1909.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

ON

Ontological on AmanahRaya Real Estate Investment Trust ·

Income Focused ARREIT

Fair Value:RM 0.2190.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OO

OOO97 on QXO ·

QXO aims for $24B revenue by 2031 with AI-driven margin expansion (Priced for good execution)

Fair Value:US$32.5357.1% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Sonic Healthcare ·

Sonic Healthcare is poised for large upside as margins recover

Fair Value:AU$2723.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.2% undervalued

98 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.1% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.8% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0