Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Socfinaf S.A. (BDL:SOFAF) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does Socfinaf Carry?

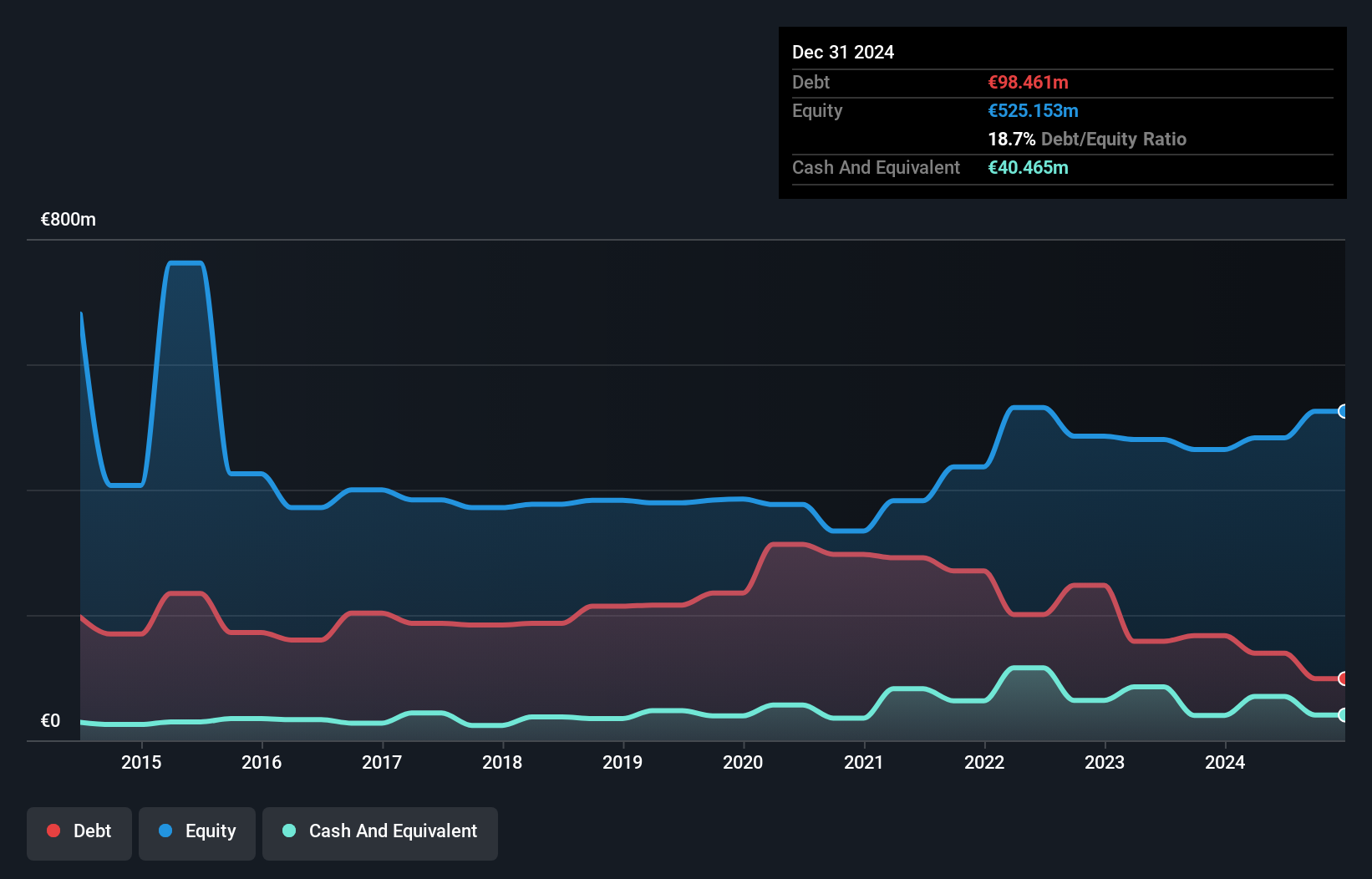

You can click the graphic below for the historical numbers, but it shows that Socfinaf had €98.5m of debt in December 2024, down from €166.9m, one year before. On the flip side, it has €40.5m in cash leading to net debt of about €58.0m.

A Look At Socfinaf's Liabilities

We can see from the most recent balance sheet that Socfinaf had liabilities of €166.7m falling due within a year, and liabilities of €106.7m due beyond that. Offsetting this, it had €40.5m in cash and €50.5m in receivables that were due within 12 months. So its liabilities total €182.4m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Socfinaf is worth €330.0m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

View our latest analysis for Socfinaf

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Socfinaf has a low net debt to EBITDA ratio of only 0.33. And its EBIT easily covers its interest expense, being 11.0 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, Socfinaf grew its EBIT by 5.0% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But it is Socfinaf's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Socfinaf recorded free cash flow worth a fulsome 81% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Our View

Socfinaf's conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But truth be told we feel its level of total liabilities does undermine this impression a bit. When we consider the range of factors above, it looks like Socfinaf is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. Over time, share prices tend to follow earnings per share, so if you're interested in Socfinaf, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BDL:SOFAF

Socfinaf

Through its subsidiaries, primarily engages in the production, processing, and sale of palm oil in Sierra Leone, Liberia, Côte d'Ivoire, Ghana, Nigeria, Cameroon, São Tomé and Principe, Congo, and Europe.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|12.0% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|5.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor