Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSE:A192650

Some Investors May Be Worried About DREAMTECH's (KRX:192650) Returns On Capital

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. However, after investigating DREAMTECH (KRX:192650), we don't think it's current trends fit the mold of a multi-bagger.

What is Return On Capital Employed (ROCE)?

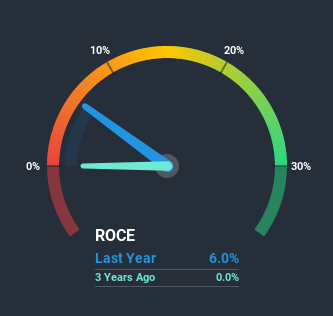

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for DREAMTECH:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.06 = ₩20b ÷ (₩604b - ₩277b) (Based on the trailing twelve months to December 2020).

Thus, DREAMTECH has an ROCE of 6.0%. On its own that's a low return on capital but it's in line with the industry's average returns of 5.7%.

See our latest analysis for DREAMTECH

Above you can see how the current ROCE for DREAMTECH compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering DREAMTECH here for free.

So How Is DREAMTECH's ROCE Trending?

We weren't thrilled with the trend because DREAMTECH's ROCE has reduced by 74% over the last two years, while the business employed 82% more capital. Usually this isn't ideal, but given DREAMTECH conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. The funds raised likely haven't been put to work yet so it's worth watching what happens in the future with DREAMTECH's earnings and if they change as a result from the capital raise.

On a separate but related note, it's important to know that DREAMTECH has a current liabilities to total assets ratio of 46%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

In Conclusion...

In summary, despite lower returns in the short term, we're encouraged to see that DREAMTECH is reinvesting for growth and has higher sales as a result. And the stock has followed suit returning a meaningful 85% to shareholders over the last year. So while the underlying trends could already be accounted for by investors, we still think this stock is worth looking into further.

DREAMTECH does have some risks, we noticed 5 warning signs (and 1 which is a bit concerning) we think you should know about.

While DREAMTECH may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading DREAMTECH or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A192650

DREAMTECH

Engages in the design, development, and manufacture of modules in South Korea and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor