Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A148150

Revenues Not Telling The Story For Se Gyung Hi Tech Co., Ltd. (KOSDAQ:148150) After Shares Rise 29%

Se Gyung Hi Tech Co., Ltd. (KOSDAQ:148150) shares have continued their recent momentum with a 29% gain in the last month alone. Taking a wider view, although not as strong as the last month, the full year gain of 16% is also fairly reasonable.

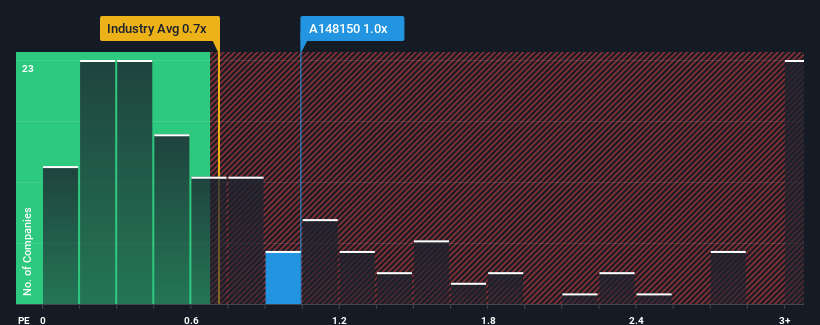

Even after such a large jump in price, there still wouldn't be many who think Se Gyung Hi Tech's price-to-sales (or "P/S") ratio of 1x is worth a mention when the median P/S in Korea's Electronic industry is similar at about 0.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Se Gyung Hi Tech

What Does Se Gyung Hi Tech's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, Se Gyung Hi Tech has been doing relatively well. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Se Gyung Hi Tech.Is There Some Revenue Growth Forecasted For Se Gyung Hi Tech?

The only time you'd be comfortable seeing a P/S like Se Gyung Hi Tech's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a decent 14% gain to the company's revenues. The latest three year period has also seen a 29% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 4.4% over the next year. Meanwhile, the rest of the industry is forecast to expand by 8.4%, which is noticeably more attractive.

With this in mind, we find it intriguing that Se Gyung Hi Tech's P/S is closely matching its industry peers. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Se Gyung Hi Tech's P/S?

Se Gyung Hi Tech's stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our look at the analysts forecasts of Se Gyung Hi Tech's revenue prospects has shown that its inferior revenue outlook isn't negatively impacting its P/S as much as we would have predicted. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. A positive change is needed in order to justify the current price-to-sales ratio.

Having said that, be aware Se Gyung Hi Tech is showing 2 warning signs in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Se Gyung Hi Tech, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A148150

Se Gyung Hi Tech

Engages in the manufacture and sale of electronic equipment parts.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor