Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A078600

Is Daejoo Electronic Materials (KOSDAQ:078600) A Future Multi-bagger?

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in Daejoo Electronic Materials' (KOSDAQ:078600) returns on capital, so let's have a look.

What is Return On Capital Employed (ROCE)?

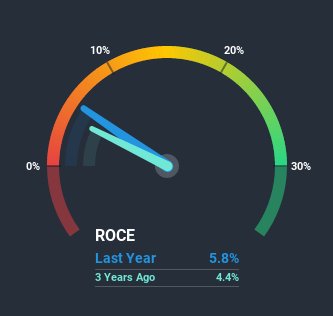

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Daejoo Electronic Materials:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.058 = ₩8.0b ÷ (₩205b - ₩67b) (Based on the trailing twelve months to September 2020).

Thus, Daejoo Electronic Materials has an ROCE of 5.8%. Even though it's in line with the industry average of 5.6%, it's still a low return by itself.

See our latest analysis for Daejoo Electronic Materials

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Daejoo Electronic Materials' past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Daejoo Electronic Materials' ROCE Trending?

We're delighted to see that Daejoo Electronic Materials is reaping rewards from its investments and is now generating some pre-tax profits. The company was generating losses five years ago, but now it's earning 5.8% which is a sight for sore eyes. Not only that, but the company is utilizing 122% more capital than before, but that's to be expected from a company trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

One more thing to note, Daejoo Electronic Materials has decreased current liabilities to 33% of total assets over this period, which effectively reduces the amount of funding from suppliers or short-term creditors. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.The Key Takeaway

In summary, it's great to see that Daejoo Electronic Materials has managed to break into profitability and is continuing to reinvest in its business. And with the stock having performed exceptionally well over the last five years, these patterns are being accounted for by investors. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

If you'd like to know more about Daejoo Electronic Materials, we've spotted 3 warning signs, and 1 of them is significant.

While Daejoo Electronic Materials may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Daejoo Electronic Materials or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A078600

Daejoo Electronic Materials

Develops and sells electronic materials in South Korea, China, Taiwan, the United States, Europe, and Southeast Asia.

Solid track record and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor