Advertisement

- South Korea

- /

- Diversified Financial

- /

- KOSDAQ:A046440

Should You Rely On KG Mobilians's (KOSDAQ:046440) Earnings Growth?

Broadly speaking, profitable businesses are less risky than unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. Today we'll focus on whether this year's statutory profits are a good guide to understanding KG Mobilians (KOSDAQ:046440).

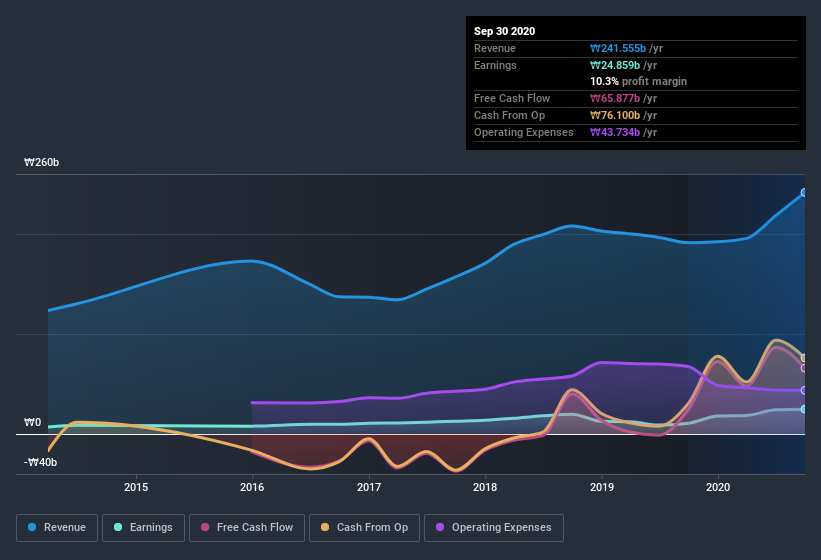

We like the fact that KG Mobilians made a profit of ₩24.9b on its revenue of ₩241.6b, in the last year. Happily, it has grown both its profit and revenue over the last three years, as you can see in the chart below.

View our latest analysis for KG Mobilians

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. So today we'll look at what KG Mobilians' cashflow tells us about its earnings, as well as examining how issuing shares is impacting shareholder value. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Zooming In On KG Mobilians' Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

KG Mobilians has an accrual ratio of -0.13 for the year to September 2020. Therefore, its statutory earnings were quite a lot less than its free cashflow. To wit, it produced free cash flow of ₩66b during the period, dwarfing its reported profit of ₩24.9b. KG Mobilians shareholders are no doubt pleased that free cash flow improved over the last twelve months. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, KG Mobilians increased the number of shares on issue by 28% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out KG Mobilians' historical EPS growth by clicking on this link.

A Look At The Impact Of KG Mobilians' Dilution on Its Earnings Per Share (EPS).

KG Mobilians has improved its profit over the last three years, with an annualized gain of 94% in that time. But EPS was only up 40% per year, in the exact same period. And at a glance the 130% gain in profit over the last year impresses. On the other hand, earnings per share are only up 24% in that time. So you can see that the dilution has had a fairly significant impact on shareholders.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So KG Mobilians shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On KG Mobilians' Profit Performance

In conclusion, KG Mobilians has strong cashflow relative to earnings, which indicates good quality earnings, but the dilution means its earnings per share growth is weaker than its profit growth. Based on these factors, it's hard to tell if KG Mobilians' profits are a reasonable reflection of its underlying profitability. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. For example, we've discovered 2 warning signs that you should run your eye over to get a better picture of KG Mobilians.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade KG Mobilians, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if KG Mobilians might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A046440

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor