Advertisement

- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A089790

JT's (KOSDAQ:089790) Shareholders Have More To Worry About Than Only Soft Earnings

The subdued market reaction suggests that JT Corporation's (KOSDAQ:089790) recent earnings didn't contain any surprises. We think that investors are worried about some weaknesses underlying the earnings.

Check out our latest analysis for JT

Examining Cashflow Against JT's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

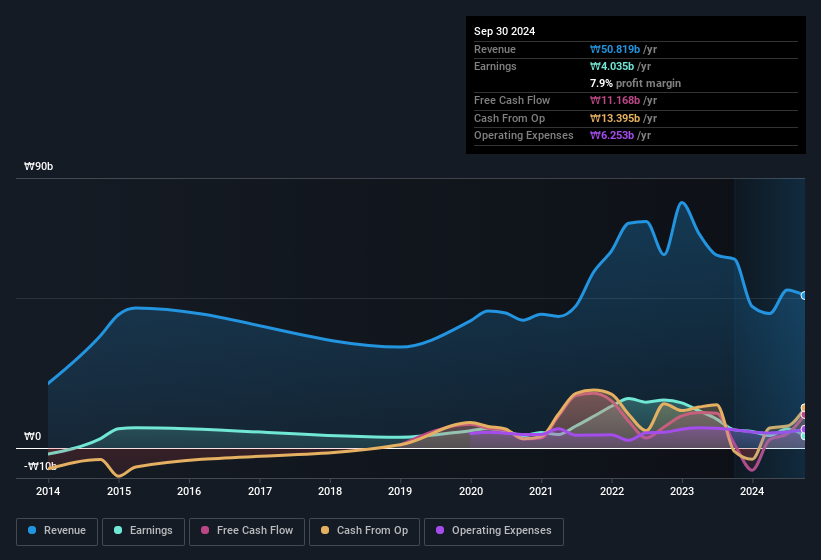

JT has an accrual ratio of -0.23 for the year to September 2024. Therefore, its statutory earnings were very significantly less than its free cashflow. In fact, it had free cash flow of ₩11b in the last year, which was a lot more than its statutory profit of ₩4.04b. JT's free cash flow improved over the last year, which is generally good to see. Having said that it seems that a recent tax benefit and some unusual items have impacted its profit (and this its accrual ratio).

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of JT.

The Impact Of Unusual Items On Profit

Surprisingly, given JT's accrual ratio implied strong cash conversion, its paper profit was actually boosted by ₩1.5b in unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. We can see that JT's positive unusual items were quite significant relative to its profit in the year to September 2024. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

An Unusual Tax Situation

Moving on from the accrual ratio, we note that JT profited from a tax benefit which contributed ₩357m to profit. This is meaningful because companies usually pay tax rather than receive tax benefits. Of course, prima facie it's great to receive a tax benefit. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

Our Take On JT's Profit Performance

Summing up, JT's accrual ratio suggests that its statutory earnings are well matched by free cash flow while its unusual items and tax benefit is boosted profit in a way that may not be sustained. Based on these factors, we think that JT's statutory profits probably make it seem better than it is on an underlying level. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. In terms of investment risks, we've identified 2 warning signs with JT, and understanding these should be part of your investment process.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A089790

JT

Engages in the research, development, and sale of semiconductor process and automation equipment in South Korea and internationally.

Adequate balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor