Advertisement

- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A074600

The Market Doesn't Like What It Sees From Wonik QnC Corporation's (KOSDAQ:074600) Earnings Yet

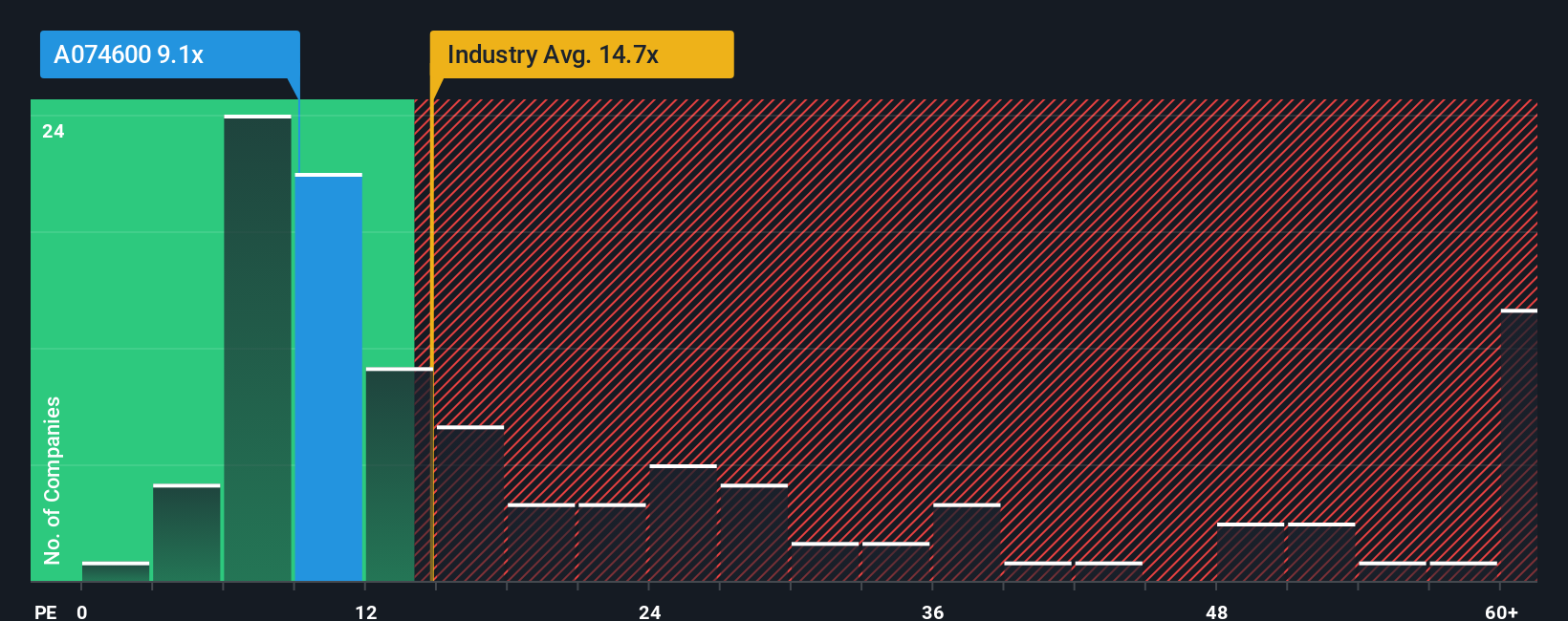

Wonik QnC Corporation's (KOSDAQ:074600) price-to-earnings (or "P/E") ratio of 9.1x might make it look like a buy right now compared to the market in Korea, where around half of the companies have P/E ratios above 14x and even P/E's above 30x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times have been advantageous for Wonik QnC as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Wonik QnC

Is There Any Growth For Wonik QnC?

There's an inherent assumption that a company should underperform the market for P/E ratios like Wonik QnC's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 34% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 18% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 17% as estimated by the three analysts watching the company. Meanwhile, the broader market is forecast to expand by 28%, which paints a poor picture.

In light of this, it's understandable that Wonik QnC's P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Wonik QnC's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Wonik QnC's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 1 warning sign for Wonik QnC you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Wonik QnC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A074600

Wonik QnC

Manufactures and sells quartz and ceramic wares used in the production of semiconductor wafers.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor