Advertisement

- India

- /

- Professional Services

- /

- NSEI:QUESS

Insider Favorites: Three High-Growth Companies With Strong Ownership

Simply Wall St

Reviewed by Simply Wall St

In a global market environment where rising U.S. Treasury yields are influencing stock performance, growth stocks have shown resilience, outpacing their value counterparts despite broader economic uncertainties. As investors navigate these conditions, companies with high insider ownership often stand out as potentially strong candidates for growth due to the confidence and commitment demonstrated by those who know the business best.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.5% | 24.6% |

| Arctech Solar Holding (SHSE:688408) | 37.8% | 25.3% |

| Medley (TSE:4480) | 34% | 30.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Pharma Mar (BME:PHM) | 11.8% | 49% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Here we highlight a subset of our preferred stocks from the screener.

Wonik QnC (KOSDAQ:A074600)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Wonik QnC Corporation manufactures and sells quartz and ceramic wares for semiconductor wafer production, with a market cap of ₩616.45 billion.

Operations: The company's revenue segments include MOMQ at ₩472.48 billion, Ceramic at ₩17.21 billion, Cleaning at ₩90.75 billion, and Quartz Ware from Korea, Taiwan, Germany, and the United States contributing ₩200.87 billion, ₩45.46 billion, ₩28.40 billion, and ₩15.73 billion respectively.

Insider Ownership: 19.6%

Earnings Growth Forecast: 34.1% p.a.

Wonik QnC shows potential as a growth company with high insider ownership, with earnings forecasted to grow significantly at 34.1% annually, outpacing the Korean market average. Despite trading at nearly 60% below its estimated fair value, concerns arise from low return on equity forecasts and insufficient interest coverage by earnings. Recent financial results indicate stable net income and earnings per share growth, although revenue growth remains moderate compared to high-growth benchmarks.

- Dive into the specifics of Wonik QnC here with our thorough growth forecast report.

- According our valuation report, there's an indication that Wonik QnC's share price might be on the cheaper side.

Aptus Value Housing Finance India (NSEI:APTUS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Aptus Value Housing Finance India Limited, along with its subsidiary, operates as a housing finance company in India with a market cap of ₹174.19 billion.

Operations: The company's revenue primarily comes from providing long-term housing finance, loans against property, and refinance loans, totaling ₹10.46 billion.

Insider Ownership: 25.2%

Earnings Growth Forecast: 18% p.a.

Aptus Value Housing Finance India demonstrates growth potential with earnings forecasted to grow 18% annually, surpassing the Indian market average. Despite a price-to-earnings ratio of 27.2x, below the market's 32x, its dividend yield of 1.43% isn't well-covered by free cash flows. Recent financial activities include raising INR 4 billion through fixed-income offerings and appointing new auditors, indicating strategic financial management amidst growing revenue and net income figures for Q1 2024.

- Get an in-depth perspective on Aptus Value Housing Finance India's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Aptus Value Housing Finance India shares in the market.

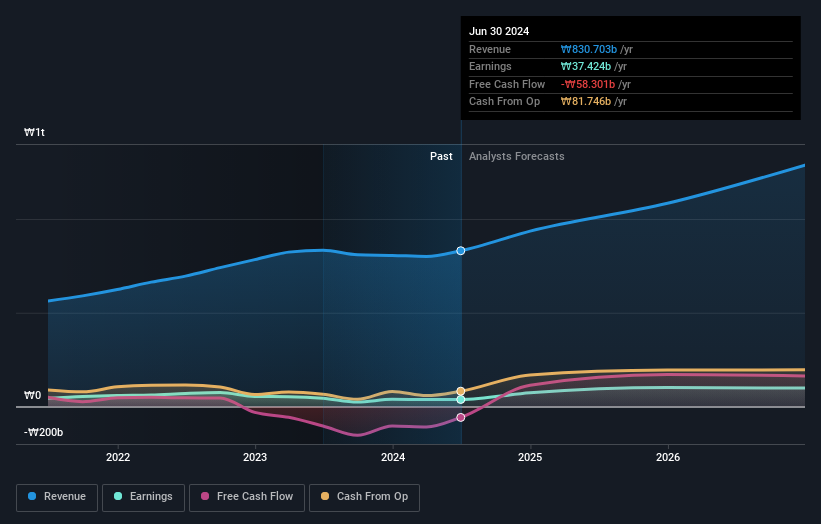

Quess (NSEI:QUESS)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Quess Corp Limited is a business services provider operating in India, South East Asia, the Middle East, and North America with a market cap of ₹103.96 billion.

Operations: The company's revenue segments include Product Led Business at ₹3.25 billion, Workforce Management at ₹142.76 billion, Operating Asset Management at ₹29.06 billion, and Global Technology Solutions (excluding Product Led Business) at ₹24.27 billion.

Insider Ownership: 15.8%

Earnings Growth Forecast: 24.4% p.a.

Quess Corp Limited shows strong growth potential with earnings expected to grow significantly at 24.4% annually, outpacing the Indian market. The company reported a notable increase in net income to INR 923.89 million for Q2 2024, reflecting a substantial year-on-year rise. Despite trading at a discount of 35% below its estimated fair value and having no recent substantial insider trading activity, its dividend track record remains unstable.

- Unlock comprehensive insights into our analysis of Quess stock in this growth report.

- The valuation report we've compiled suggests that Quess' current price could be quite moderate.

Key Takeaways

- Discover the full array of 1466 Fast Growing Companies With High Insider Ownership right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Quess might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:QUESS

Quess

Provides staffing and workforce solutions in India and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Pagaya Technologies ·

The "Rate Cut" Supercycle Winner – Profitable & Accelerating

Fair Value:US$170.685.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$16.3254.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

110 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

943 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative